The market spotlight was focused on U.S. top-tier events for the day, namely the CPI release and Fed statement, and these catalysts did not disappoint when it came to volatility.

Both major market movers had some surprises, which then triggered big swings for dollar pairs and risk assets.

Read on to find out what happened!

Headlines:

- China’s headline CPI in May: 0.3% y/y (0.4% forecast, 0.3% previous)

- China’s PPI in May: -1.4% y/y (-1.5% forecast, -2.5% previous)

- U.K. GDP in April: 0.0% m/m (0.0% forecast, 0.4% previous)

- U.K. goods trade deficit in April: -19.6B GBP (-14.2B GBP forecast, -14.0B GBP previous)

- U.K. industrial production slumped 0.9% m/m in April, manufacturing production down 1.4% (projected 0.2% dip, previous 0.3% uptick)

- U.S. Department of Energy sees global oil demand rising by 1.1 million barrels per day this year vs. previous estimate of 900 million barrels per day

- U.S. headline CPI in May: 0.0% (0.1% expected, 0.3% previous), annual reading down from 3.4% to 3.3% (3.4% consensus)

- U.S. core CPI in May: 0.2% m/m (0.3% expected, 0.3% previous)

- EIA crude oil inventories rose by 3.7 million barrels vs. estimated reduction of 1.2 million barrels

- FOMC kept interest rates on hold at 5.25-5.50% as expected, noted “modest further progress” in inflation

- Fed dot plot projections signaled scope for one rate cut this year, down from previous estimate of three reductions

- Fed head Powell stressed data-dependent approach when it comes to timing of easing, adds that inflation has eased but still too high

- BOC Governor Macklem noted that monetary policy no longer needs to be as restrictive as it had been

- U.K. RICS house price balance in May: -17% (-5% consensus, -7% previous)

- Japan’s BSI manufacturing index in Q2: -1.0 (-5.2 forecast, -6.7 previous)

Broad Market Price Action:

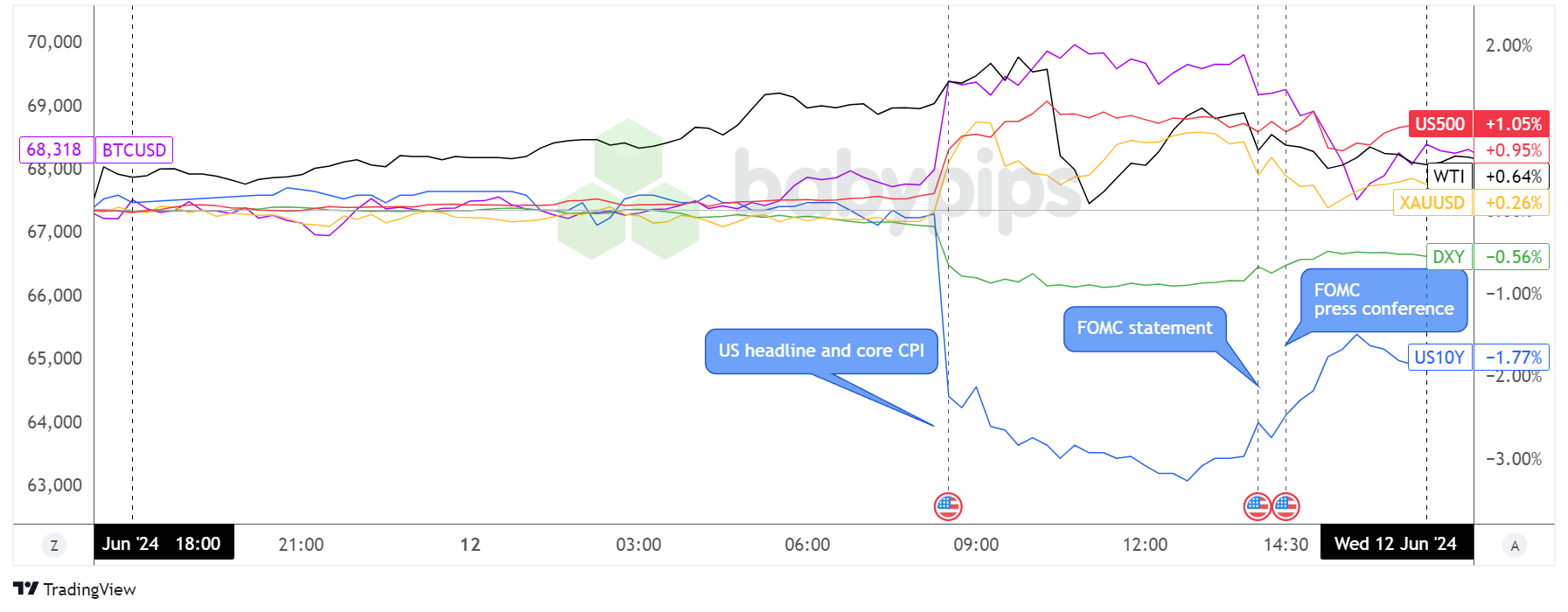

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

The calm before the CPI storm was pretty evident during the Asian and London sessions, as most asset classes were in consolidation leading up to the top-tier U.S. news release.

Crude oil was an exception, though, as the commodity slowly crawled higher, possibly still enjoying the bullish vibes from upgraded global oil demand forecasts from the Department of Energy. It gave up majority of its gains when the EIA report printed a surprise inventory build of 3.7 million barrels instead of the expected reduction of 1.2 million barrels in inventories.

Meanwhile, other asset classes went berserk during the U.S. CPI release, as the numbers all came in the red and spurred jitters of a potential dovish FOMC statement later on. Treasury yields took a sharp hit while equities, bitcoin, and gold took advantage of the dollar selloff that ensued.

These big moves were somewhat reversed during the Fed decision, as many were surprised to see the dot plot forecasts scale down the number of potential cuts for the year from three down to just one.

U.S. bond yields extended their recovery throughout Powell’s presser while gold, bitcoin, and crude oil continued to retreat. Interestingly enough, the S&P 500 index managed to hold its ground, as investors probably turned their attention to the increase in possible rate cuts for 2025.

FX Market Behavior: U.S. Dollar vs. Majors

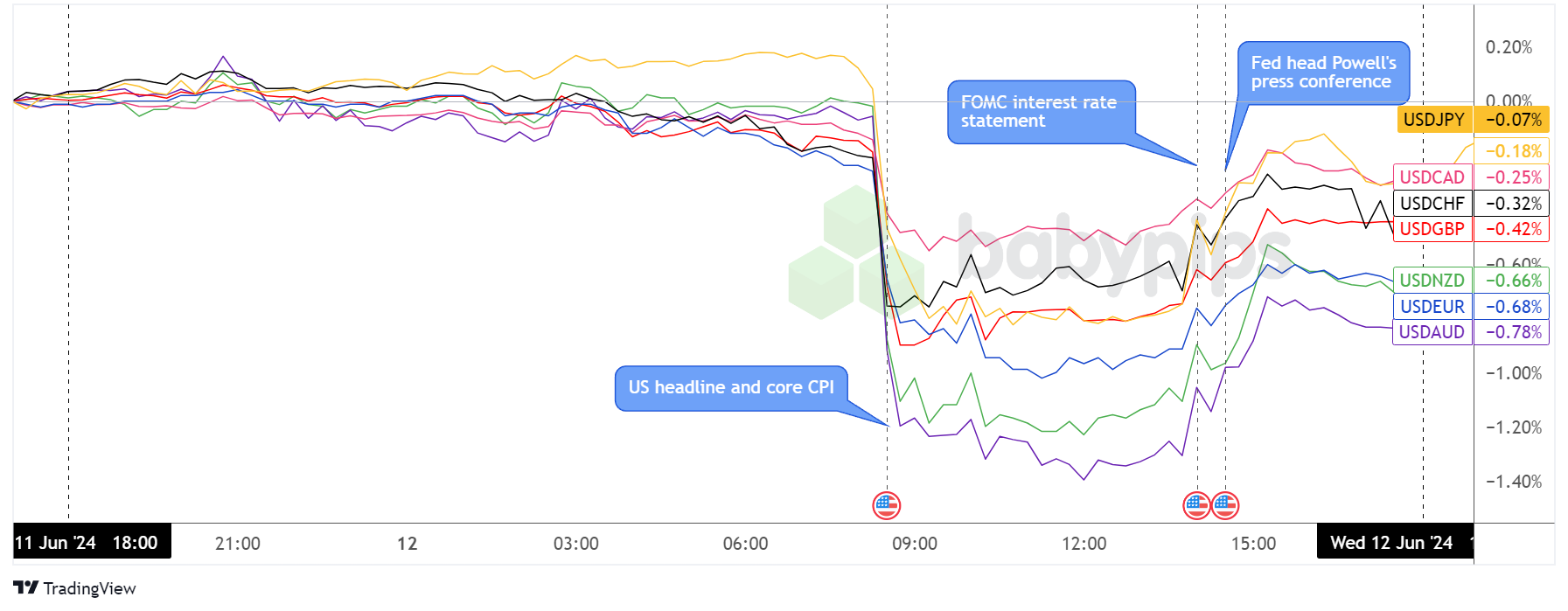

Overlay of USD vs. Major Currencies Chart by TradingView

Dollar traders were biting their nails ahead of the U.S. CPI report and Fed statement, which both came through when it comes to spurring volatility across the board.

Consolidation seemed pretty tight among the majors, although there was a slight bearish tilt for the dollar during the earlier trading sessions, except for USD/JPY. The actual CPI report spurred a sharp tumble for the U.S. currency since the numbers all fell short of estimates.

From there, price action leveled off as traders looked ahead to the incoming FOMC statement. Even though the Fed kept rates unchanged as expected, the announcement and economic projections turned out more hawkish than before, as policymakers noted “modest progress” in inflation and trimmed their potential rate cuts from three down to one this year.

The dollar was able to sustain its rebound throughout Fed head Powell’s presser, as he acknowledged that they don’t have enough confidence enough to start easing policy this time.

Upcoming Potential Catalysts on the Economic Calendar:

- Swiss PPI at 6:30 am GMT

- U.S. headline and core PPI at 12:30 pm GMT

- U.S. weekly initial jobless claims at 12:30 pm GMT

- New Zealand BusinessNZ manufacturing index at 10:30 pm GMT

- Bank of Japan’s (BOJ) monetary policy statement coming up

Another batch of top-tier data points is lined up from the U.S. economy today, although probably not as blockbuster as the latest events. Still, intraday dollar volatility is typically seen during the U.S. PPI and weekly initial jobless claims release, so better stay on your toes!

After that, we’ve got the BOJ monetary policy announcement lined up for the next Asian trading session, so the spotlight could shift to yen pairs then.

Looking for your own spot to record your market observations & trading statistics? If so, then check out TRADEZELLA! It’s an easy-to-use

journaling tool that can lead to valuable performance & strategy insights! You can easily add your thoughts, charts & track your psychology with each and every trade. Click here to see if it’s right for you!Disclaimer: Babypips.com earns a commission from any signups through our affiliate link. When you subscribe to a service using our affiliate links, this helps us to maintain and improve our content, a lot of which is free and accessible to everyone–including the School of Pipsology! We appreciate your support and hope that you find our content and services helpful. Thank you!