The Federal Open Market Committee (FOMC) maintained the target range for the federal funds rate at 5.25-5.50% as expected in their latest announcement.

Their official statement acknowledged that “there has been modest further progress toward the Committee’s 2% inflation objective” in recent months, which was more upbeat compared to the earlier rhetoric on “a lack of further progress in inflation.”

In the latest FOMC Economic Projections, the Fed maintained their median growth forecasts while upgrading inflation estimates for this year and the next.

What caught everyone’s attention was the updated dot plot projections of interest rates, as it scaled down potential interest rate cuts from three down to just one this year.

In particular, 11 out of 19 policymakers are expecting no more than one rate cut this 2024 while four officials actually expect no easing moves at all. However, the Fed dot plot also revealed more interest rate cuts in 2025, from three up to four reductions.

Link to FOMC Economic Projections

During the press conference, Fed head Powell highlighted the U.S. CPI print earlier, citing that “We see today’s report as progress and as, you know, building confidence. But we don’t see ourselves as having the confidence that would warrant beginning to loosen policy at this time.”

The CME Group’s FedWatch tool now predicts a 63% probability of a September cut, down from previous expectations of a 70% chance earlier in the day.

Market Reactions

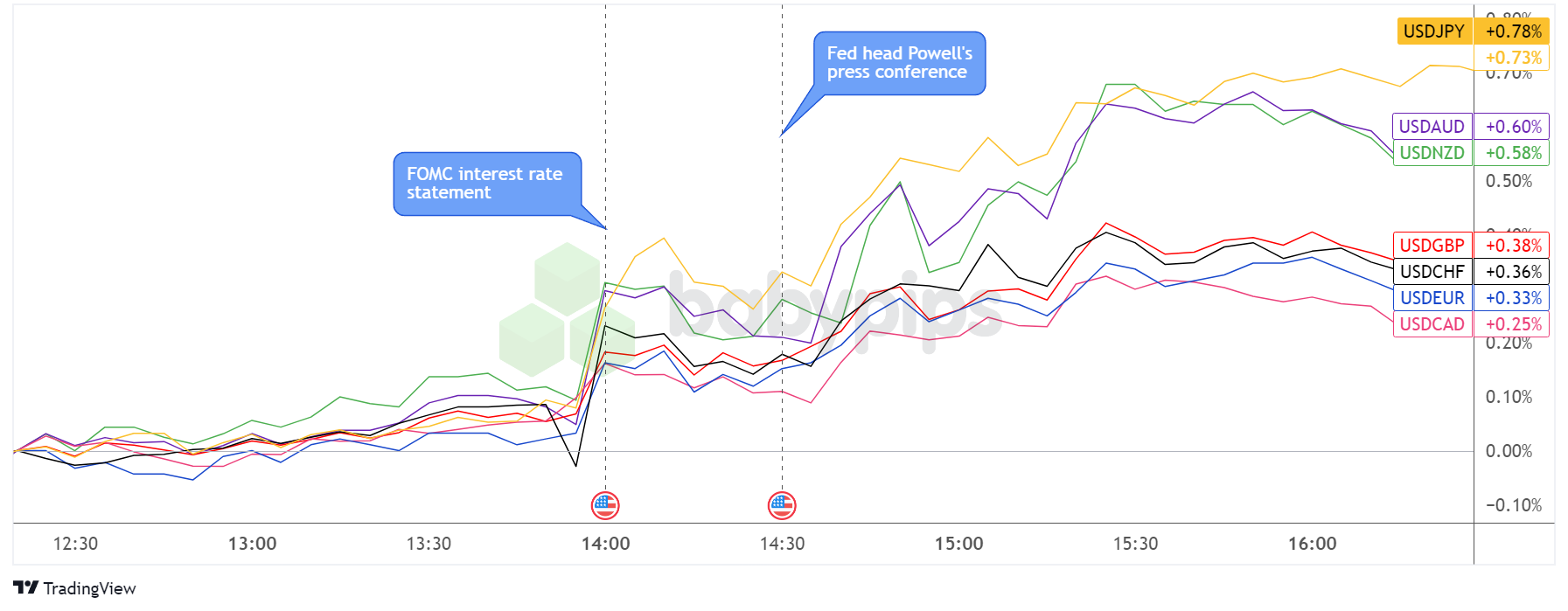

U.S. Dollar vs. Major Currencies: 5-min

Overlay of USD vs. Major Currencies Chart by TradingView

The U.S. dollar had been pulling gradually higher after its post-CPI tumble in the hours leading up to the FOMC statement.

The actual announcement was seen as mostly hawkish overall, spurring a brief rally for the Greenback likely on the reduction of planned easing moves for the remainder of the year.

A bit of sideways price action ensued as traders braced for Fed head Powell’s press conference, which then led to a more prolonged climb for the U.S. currency on the lack of dovish commentary.

The dollar chalked up its largest lead versus the Japanese yen, followed by the Aussie and Kiwi, as the higher-yielding currencies likely caved to risk-off flows.