Despite a less hawkish FOMC event on Wednesday, the U.S. dollar took the top spot among the forex majors this week.

Friday’s one-two punch of way better-than-expected U.S. jobs data and U.S. business services survey data easily lifted it back into the green and ahead of the pack into the weekend.

Notable News & Economic Updates:

IMF raised its global GDP forecast to 2.9% growth this year on China’s reopening

J.P.Morgan Global Manufacturing PMI for January: 49.1 vs. 48.7 previous; “Input cost and output price inflation both edge higher”

Chinese official manufacturing PMI rose from 47.0 to 50.1 in Jan vs. 50.2 consensus; China’s Caixin Manufacturing PMI survey improved from 49.0 to 49.2 in January

Preliminary data showed that GDP in Canada was 0.0% m/m in December vs. 0.1% m/m gain in November

New Zealand’s jobless rate ticked up from 3.3% to 3.4% in Q4, the highest in five quarters

Major Central Bank moves this week:

- The Federal Reserve raised the target interest rate range by 25 bps to 4.50% to 4.75% as expected

- The European Central Bank raised interest rates by 50 bps to 3.00% as forecasted & signaled another likely 50bps hike in March

- The Bank of England voted 7-2 for a 50 bps interest rate hike to 4.00% on Thursday; BOE Governor Bailey talked down speculation of pause or pivot ahead as well

S&P Global Price Pressures Index ticked higher to 0.4 in January vs. 0.3 in December; Global Supply Shortages Index ticked lower to 2.1 vs. 2.2 previous

An OPEC+ panel endorsed the oil producer group’s current output policy at a meeting on Wednesday, leaving production cuts agreed last year in place amid hopes of higher Chinese demand and uncertain prospects for Russian supply.

U.S. Employment Data this week:

- U.S. employers announced 102K job cuts in January, the most since 2020 – Challenger

- U.S. initial jobless claims drop from 186K to a nine-month low of 183K

- U.S. Non-Farm Payrolls surprised way higher-than-expected at 517K vs. 187K forecast; unemployment rate fell to 3.4% vs. 3.6% forecast

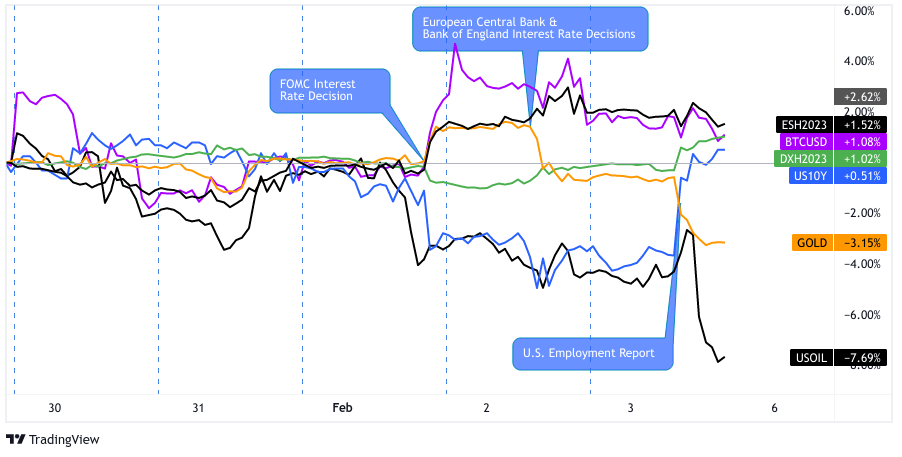

Intermarket Weekly Recap

Dollar, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay 1-Hour by TradingView

The financial markets started the busy week on a mixed note, likely on traders standing pat from taking fresh bets ahead of several interest rate decisions from major central banks and the latest U.S. employment data highlighted on Monday. There was actually a slight risk-off vibe as bond yields and the U.S. dollar started green, while risk assets dipped through the Tuesday morning session.

Risk sentiment began to improve some time late in the Tuesday session, likely on a combination of themes, including raised expectations the Fed may hint at pausing rate hikes after the market saw a dip in the U.S. Employment Cost Index. It’s also likely that the early week positive economic and sentiment reads were a factor as well, most notably the better-than-expected preliminary Eurozone GDP data and the improved Chinese PMI data.

On Wednesday, the most anticipated event of the week came and went, with the Federal Reserve raising the interest rate range target by 25 bps as expected. But Powell unexpectedly didn’t go full hawk on the markets. He noted a “most welcome” recent ease in inflation rates and shared that it hasn’t weighed the labor market…yet.

The less-hawkish-than-expected rhetoric dragged the U.S. dollar lower across the board, likely pushing gold, crypto, and U.S. equities higher. Crude oil missed the rally, however, thanks to OPEC deciding to stick to last year’s OPEC+ output cut deal amidst uncertain Chinese demand and Russian supply.

Price action was a bit more mixed near the end of the week, likely influenced by the latest interest rate decisions from the Bank of England and European Central Bank, who both raised their interest rates by 50 bps as expected.

The key takeaway was that the major central banks are staying vigilant on inflation, but are open to adjusting policy on any data points ahead showing a sustained return to their target inflation ranges. The “safe-haven” gold was dumped and U.S. and European bond yields turned sharply lower while U.S. equities tracked higher as they took cues from tech earnings releases.

Friday was a big one for the markets as the latest U.S. employment data came out with a banger of a number: +517K net job adds in January and the unemployment rate dipping to 3.4% (below 3.6% forecast). This red hot jobs number and a surprisingly positive ISM Services PMI update likely had traders pulling back odds of a “Fed Pivot” this year, characterized by a jump in bond yields and the U.S. dollar against a dip in crypto, gold and equities on the event.

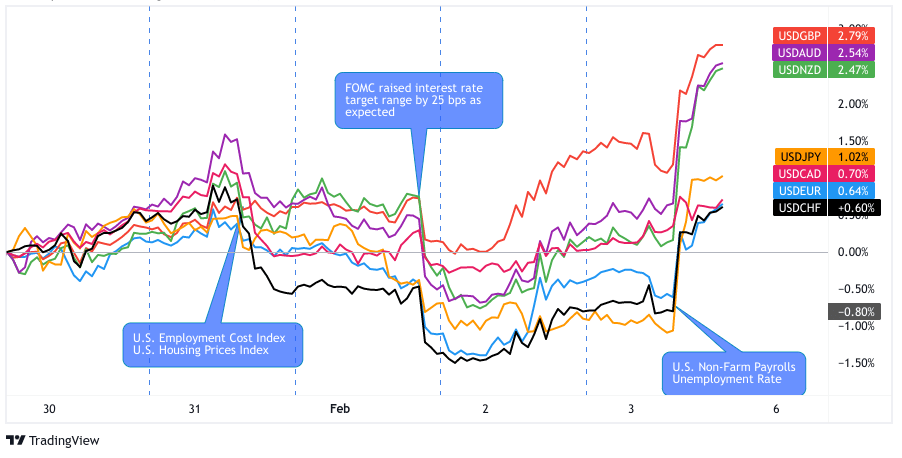

Most Notable FX Moves

USD Pairs

Overlay of USD Pairs: 1-Hour Forex Chart

U.S. Employment Cost Index came in below expectations at 1.0% vs. 1.1% forecast/1.2% previous

ADP Private Payrolls slowed to 106K in January vs. upwardly revised 253K in December

ISM U.S. Manufacturing PMI fell to 47.4 in January vs. 48.4 in December

The Federal Reserve raised interest rate range by 25 bps to 4.50% to 4.75% as expected

A preliminary read on the Q4 2022 labor costs show an increase of 1.1%, below the previous rate of 2.4%

U.S. Non-Farm Payrolls surprised way higher-than-expected at 517K vs. 187K forecast; unemployment rate fell to 3.4% vs. 3.6% forecast

ISM Services PMI for January came in way above expectations at 55.2 vs. 50.5 forecast and 49.6 in December

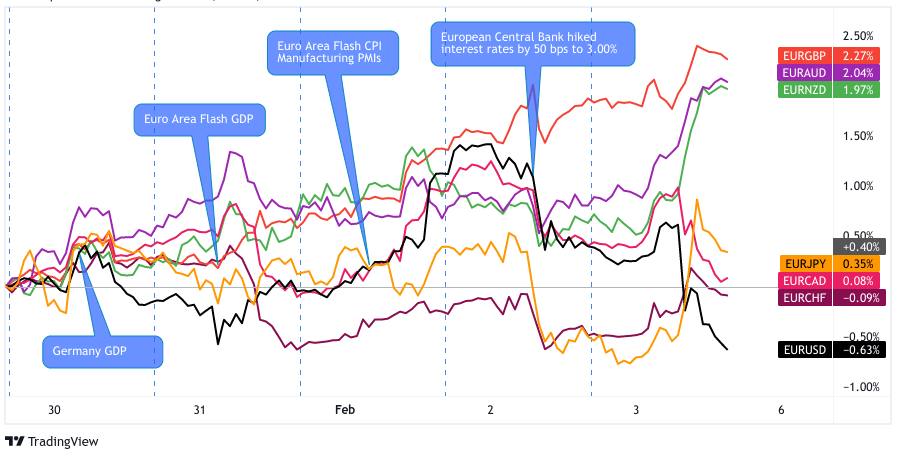

EUR Pairs

Overlay of EUR Pairs: 1-Hour Forex Chart

Germany’s GDP unexpectedly contracted by 0.2% in Q4 vs. 0.5% growth in Q3, annual growth slowed down from 1.3% to 1.1%

Euro area preliminary GDP for Q4 2022: +0.1% q/q; 0.0% q/q for the European Union

French flash GDP showed 0.1% growth q/q in Q4 vs. estimated flat reading

Eurozone Manufacturing PMI for January: 48.8 vs. 47.8 in December

As expected, the European Central Bank raised interest rates by 50 bps to 3.00% & signaled another likely 50bps hike in March

On Friday, ECB members Kazimir, Simkus and Wunsch reiterated the party line that the March 50 bps hike will not likely be the last from the European Central Bank

Germany Services PMI moved higher in January to 50.7 vs. 49.2 previous

Euro area Industrial Producer Prices were up by 1.1% y/y in December 2022; +1.2% y/y in the European Union

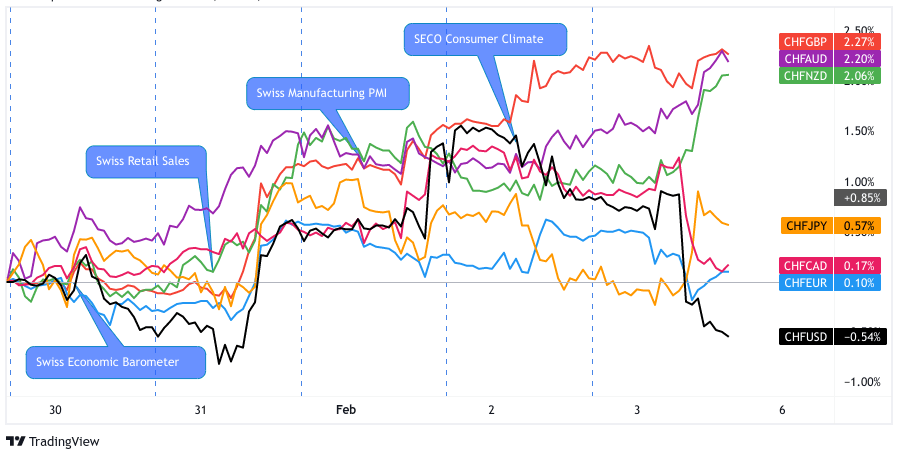

CHF Pairs

Overlay of CHF Pairs: 1-Hour Forex Chart

Switzerland’s leading KOF economic barometer up from 91.5 to 7-month high of 97.2 in January

Swiss retail sales slowed by 2.8% y/y vs. estimated 0.7% drop in Dec

Swiss Manufacturing PMI for January 2023 fell to contractionary conditions: 49.3 vs. 54.1 in December

SECO Swiss Consumer Climate Survey Index rose to -30 in January vs. -47 in December

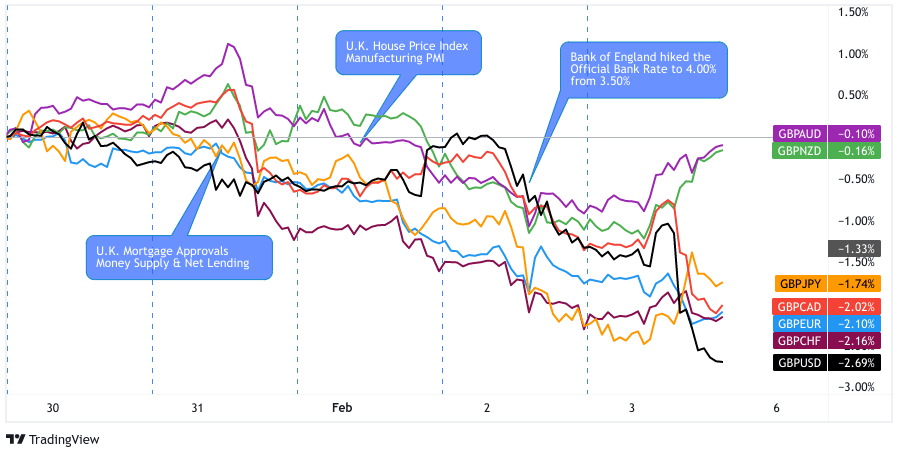

GBP Pairs

Overlay of GBP Pairs: 1-Hour Forex Chart

The British pound was the big loser of the week, likely on a combination of weak manufacturing PMI data and the results of Thursday’s Bank of England monetary policy event.

The Bank of England voted 7-2 for a 50 bps interest rate hike to 4.00% on Thursday

While Governor Bailey did mention signs of a potential peak in inflation rates, he also reiterated that the BOE would continue to tighten until they were “absolutely sure” inflation was cooling down, likely fueling recession speculation ahead for the U.K.