Dollar domination was the name of the game, as risk-off vibes lifted the safe-haven currency across the board while dragging commodities south.

Stronger than expected inflation data gave the Aussie a fighting chance, though.

Read on to find out how the rest of the majors and asset classes turned out!

Headlines:

- Australia’s MI leading index for May stayed flat

- Australia’s headline CPI for May: 4.0% y/y (3.8% expected, 3.6% previous)

- German GfK consumer climate index for June: -21.8 (-19.4 expected, -21.0 previous)

- Swiss UBS economic expectations index for May: 17.5 (18.2 previous)

- U.K. CBI realized sales for May: -24 (+1 expected, +8 previous)

- U.S. new home sales for May: 619K (636K expected, previous reading upgraded from 634K to 698K)

- EIA crude oil inventories: +3.6 million barrels (-2.6 million barrels expected, -2.5 million barrels previous)

- Japanese retail sales in May: 3.0% y/y (2.0% expected, previous reading downgraded from 2.4% to 2.0%)

Broad Market Price Action:

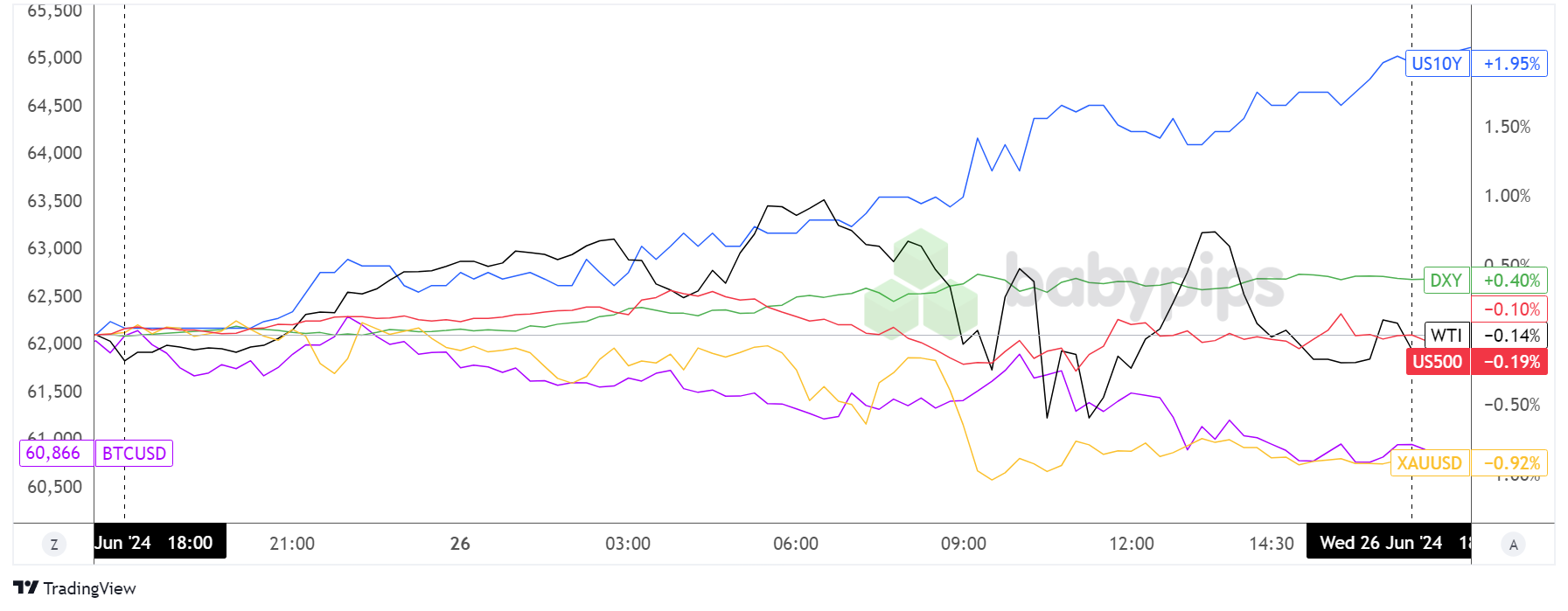

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Risk sentiment and dollar strength appeared to be the main driving forces in the financial markets in the latest trading sessions, as safe-havens advanced while higher-yielding assets like gold and bitcoin tumbled throughout the day.

WTI crude oil initially had a solid lead before it erased its gains when the EIA crude oil inventory report printed a surprise build in stockpiles, suggesting weaker demand conditions.

The S&P 500 index also struggled to stay afloat but was unable to stay in the green, even after a handful of tech sector stocks like TSLA and AMZN chalked up some winnings. On the flip side, bond yields were on a steady climb as the 5-year auction led to a selloff in Treasuries.

FX Market Behavior: U.S. Dollar vs. Majors

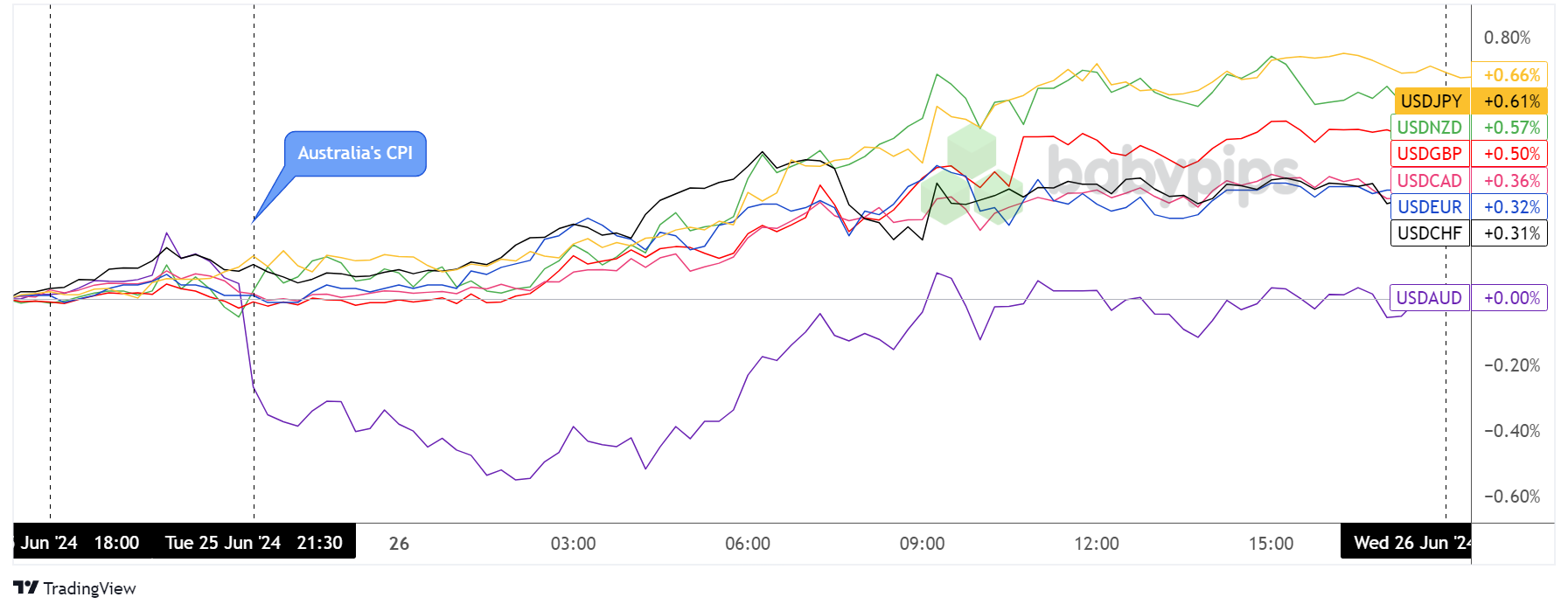

Overlay of USD vs. Major Currencies Chart by TradingView

The Greenback cruised higher against majority of its counterparts the entire day, with the exception of the Australian dollar which was able to benefit from an upside surprise in CPI figures.

Still, AUD/USD wound up returning its post-CPI gains, as risk aversion took hold of the markets as the London session went on.

Meanwhile, USD/JPY’s rally past the 160.00 major psychological mark kept traders wary of currency intervention, but the lack of any moves from the BOJ kept the yen pair above this key level.

Upcoming Potential Catalysts on the Economic Calendar:

- BOE Financial Stability Report at 9:00 am GMT

- BOE Governor Bailey’s speech at 9:30 am GMT

- U.S. final GDP reading for Q1 2024 at 12:30 pm GMT

- U.S. initial jobless claims at 12:30 pm GMT

- U.S. durable goods orders data at 12:30 pm GMT

- U.S. pending home sales at 2:00 pm GMT

- Tokyo core CPI at 11:30 am GMT

- Japanese jobless rate at 11:30 am GMT

- Japanese industrial production at 11:30 am GMT

The market spotlight could stay on the U.S. dollar today, as Uncle Sam is scheduled to print the final version of its Q1 GDP along with the weekly initial jobless claims report which tends to spark strong intraday volatility.

Be sure to stay on your toes for more profit-taking activity near the end of the week AND month AND quarter, too!

Looking for your own spot to record your market observations & trading statistics? If so, then check out TRADEZELLA! It’s an easy-to-use

journaling tool that can lead to valuable performance & strategy insights! You can easily add your thoughts, charts & track your psychology with each and every trade. Click here to see if it’s right for you!Disclaimer: Babypips.com earns a commission from any signups through our affiliate link. When you subscribe to a service using our affiliate links, this helps us to maintain and improve our content, a lot of which is free and accessible to everyone–including the School of Pipsology! We appreciate your support and hope that you find our content and services helpful. Thank you!