The market spotlight was focused on a couple of major central bank announcements, with one delivering a surprise rate cut.

How did the rest of the asset classes fare?

Headlines:

- People’s Bank of China kept 1-year and 5-year prime loan rates unchanged at 3.45% and 3.95% respectively

- Swiss trade surplus in May: 5.81 billion CHF (3.84 billion CHF forecast, 4.34 billion CHF previous) as exports fell 1.6% while imports slumped 3.8%

- German PPI in May: 0.0% m/m (0.1% expected, 0.2% previous)

- Swiss National Bank (SNB) cut interest rates by 25 bps to 1.25% vs. expectations of keeping rates steady at 1.50%, noted franc appreciation in past weeks and risks to inflation development

- Bank of England (BOE) kept interest rates on hold at 5.25% as expected in 7-2 MPC vote, but members noted that August decision is a ‘live’ one

- U.S. weekly initial jobless claims: 238K (235K expected, 243K previous)

- U.S. building permits in May: 1.39M (1.45M expected, 1.44M previous)

- U.S. housing starts in May: 1.28M (1.37M expected, 1.35M previous)

- Philly Fed manufacturing index in June: 1.3 (4.8 expected, 4.5 previous)

- EIA crude oil inventories: -2.5M barrels (-2.8M expected, +3.7M previous)

- Australian flash manufacturing PMI in June: 47.5 (49.7 previous)

- Australian flash services PMI in June: 51.0 (52.5 previous)

- U.K. GfK consumer confidence index in June: -14 (-16 expected, -17 previous)

Broad Market Price Action:

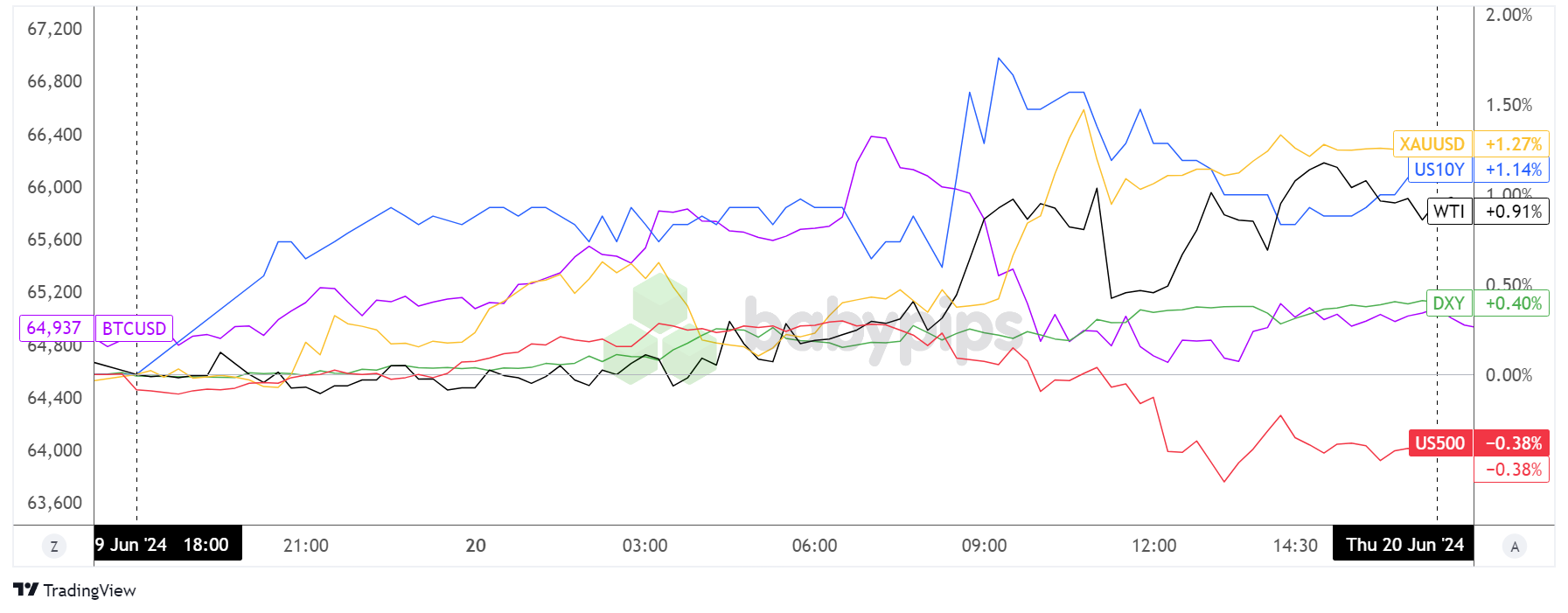

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Market participants seemed to be hungry for some risk during the Asian market hours, as gold and bitcoin edged higher while the S&P 500 index extended its climb.

Crude oil was trading sideways, though, before the energy commodity eventually popped higher on seeing a decline of 2.5 million barrels in EIA inventories.

The tide turned for U.S. equities during the New York session, as the S&P 500 index closed 0.2% lower after reaching a new high at 5,500 earlier in the day.

The Nasdaq also retreated after tech giant Nvidia reversed its previous gains and wound up 3.5% lower, trailing the likes of Microsoft and Apple as investors likely booked profits off the tech sector rallies during the first half of this week.

FX Market Behavior: U.S. Dollar vs. Majors

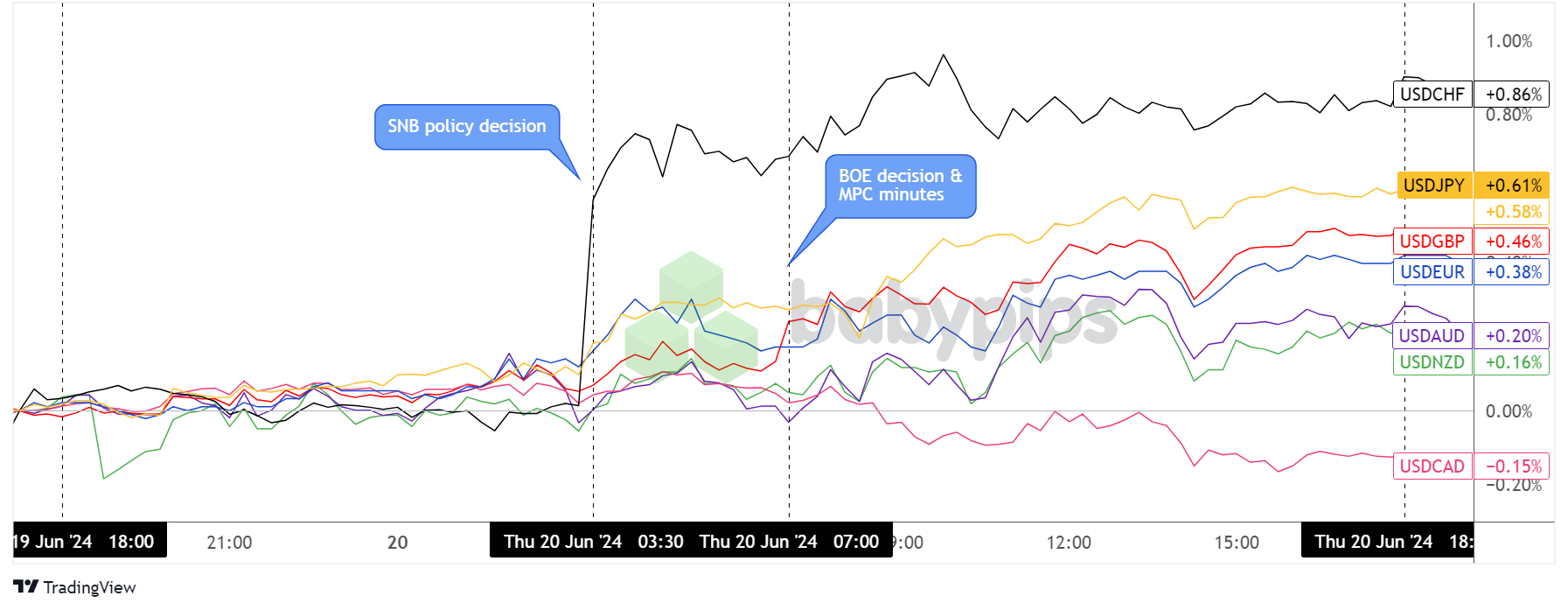

Overlay of USD vs. Major Currencies Chart by TradingView

Dollar price action was mostly sideways but slightly in the green during the early Asian session, with the exception of a slight pop higher by the Kiwi.

Volatility picked up for USD/CHF during the SNB policy statement when the central bank surprised the markets with another 0.25% interest rate cut. The pair was able to sustain its climb at a slower pace in the hours that followed, before consolidating throughout the U.S. session while still ending 0.86% higher for the day.

Cable also chalked up decent moves following the BOE’s “dovish hold” decision, as policymakers appeared to tee up a potential cut for August.

Despite mostly downbeat data from the U.S. economy, the dollar held on to its safe-haven gains versus majority of its counterparts, except for the Loonie which likely took advantage of higher crude oil prices.

Upcoming Potential Catalysts on the Economic Calendar:

- U.K. retail sales at 6:00 am GMT

- French flash manufacturing and services PMI at 7:15 am GMT

- German flash manufacturing and services PMI at 7:30 am GMT

- Eurozone flash manufacturing and services PMI at 8:00 am GMT

- U.K. flash manufacturing and services PMI at 8:30 am GMT

- Canada’s headline and core retail sales at 12:30 pm GMT

- U.S. flash manufacturing and services PMI at 1:45 pm GMT

- U.S. existing home sales at 2:00 pm GMT

Today is all about global flash PMI figures, as these leading economic indicators are likely to impact the overall market mood for the trading day. General improvements are expected in Europe, but Uncle Sam might report dips in both manufacturing and services sector activity.

Make sure you keep an eye out for potential surprises in data, as well as possible divergences in industry performance among major economies!

Looking for your own spot to record your market observations & trading statistics? If so, then check out TRADEZELLA! It’s an easy-to-use

journaling tool that can lead to valuable performance & strategy insights! You can easily add your thoughts, charts & track your psychology with each and every trade. Click here to see if it’s right for you!Disclaimer: Babypips.com earns a commission from any signups through our affiliate link. When you subscribe to a service using our affiliate links, this helps us to maintain and improve our content, a lot of which is free and accessible to everyone–including the School of Pipsology! We appreciate your support and hope that you find our content and services helpful. Thank you!