Weaker-than-expected retail activity in the U.S. drew in growth concerns and lowkey weighed on the U.S. dollar.

So why did U.S. stocks extend their gains?

Here are the headlines you need to know if you missed yesterday’s trading!

Headlines:

- RBA kept its rates at 4.35% and highlighted increased inflation risks in June

- BOJ Gov. Ueda told parliament that “there’s a chance” for a rate hike at their July meeting

- Euro Area’s final inflation rate confirmed at 2.6% y/y in May; Core CPI remains at 2.9% y/y for the month

- Euro Area ZEW economic sentiment improved from 47.0 to 51.3 in June (vs. 47.8 forecast)

- Germany’s ZEW economic sentiment increased from 47.1 to 47.5 in June (vs. 49.6 forecast); Inflation expectations rose after a higher-than-expected CPI in May

- U.S. retail sales grew by 0.1% m/m (vs. 0.3% forecast, -0.2% previous); Core retail sales fell by another 0.1% m/m in May (vs. +0.2% forecast)

- U.S. industrial production shot up by 0.9% m/m in May (vs. 0.3% forecast, 0.0% previous); Capacity utilization rate improved from 78.2% to 78.7%

- Voting FOMC member Thomas Barkin believes we’re seeing the “back side of inflation” but still wants to “learn a lot more [about inflation] over the next several months”

- Voting FOMC member Adriana Kugler supports “easing policy sometime later this year” if the economy evolves as expected

- Australia’s CB Leading Economic Index slipped by another 0.3% m/m in April; The LEI points to “headwinds to growth” after a subdued Q1 2024 GDP

- New Zealand’s Global Dairy Trade auction yielded a 0.5% dip in dairy prices following a 1.7% increase earlier this month

Broad Market Price Action:

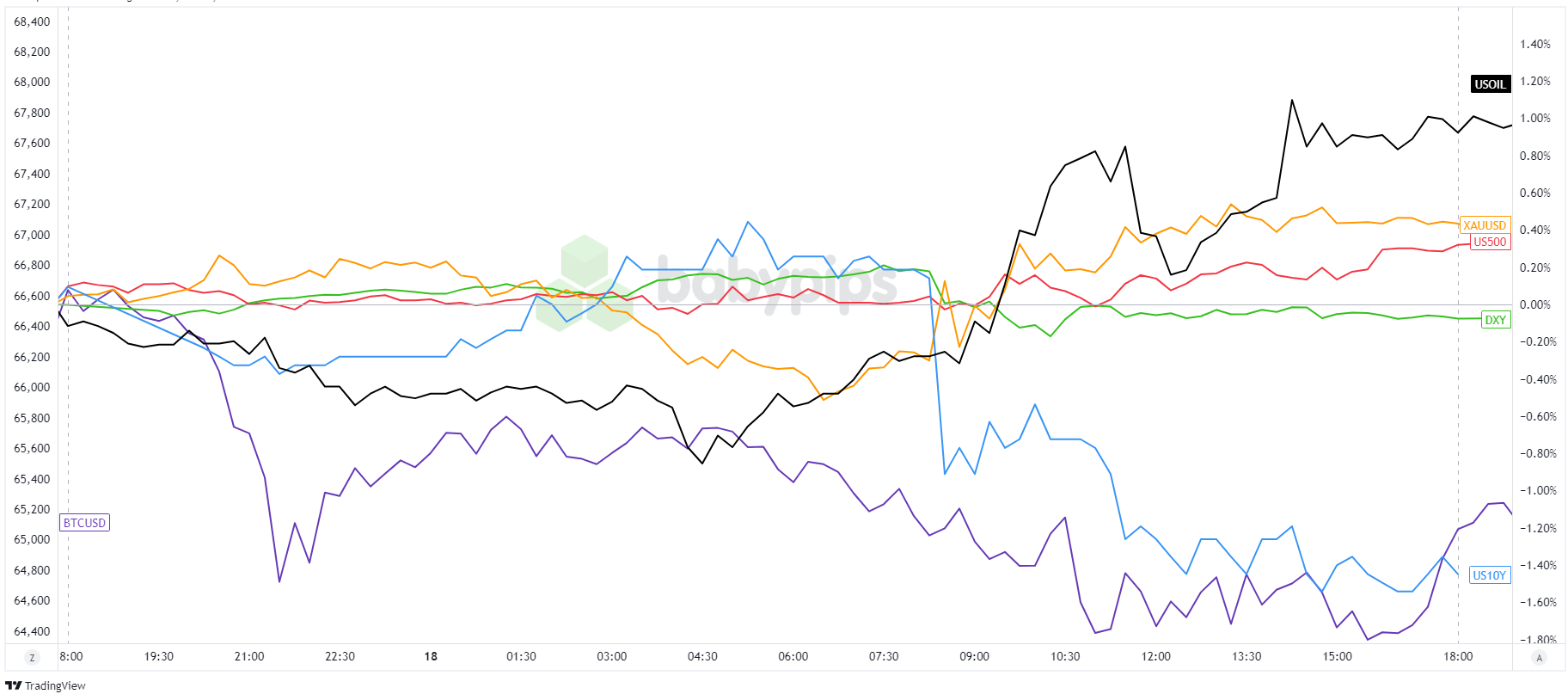

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Market activity remained muted due to a lack of fresh, market-moving news, leading major assets to react primarily to specific headlines.

Crude oil prices continued to rise, with WTI crude consistently trading above the key $80.00 level. This upswing is driven by expectations of increased demand during the summer driving season and anticipated supply cuts later in the year.

Gold temporarily lost its luster during a risk-on European trading session but rebounded after weak U.S. retail sales data dragged down U.S. Treasury yields and reduced demand for the USD. Meanwhile, bitcoin (BTC/USD) dipped to new weekly lows near $64,000 before bouncing back above $65,000.

Global equities also mostly extended their bullish runs. Asian markets were buoyed by the RBA keeping its policies steady despite rising inflation risks, while European stocks were supported by optimism about upcoming economic data and easing political concerns.

In the U.S., the S&P 500 and NASDAQ indices reached new record highs, with Nvidia surpassing Microsoft as the world’s most valuable public company, boasting a market cap of $3.22 trillion.

FX Market Behavior: U.S. Dollar vs. Majors

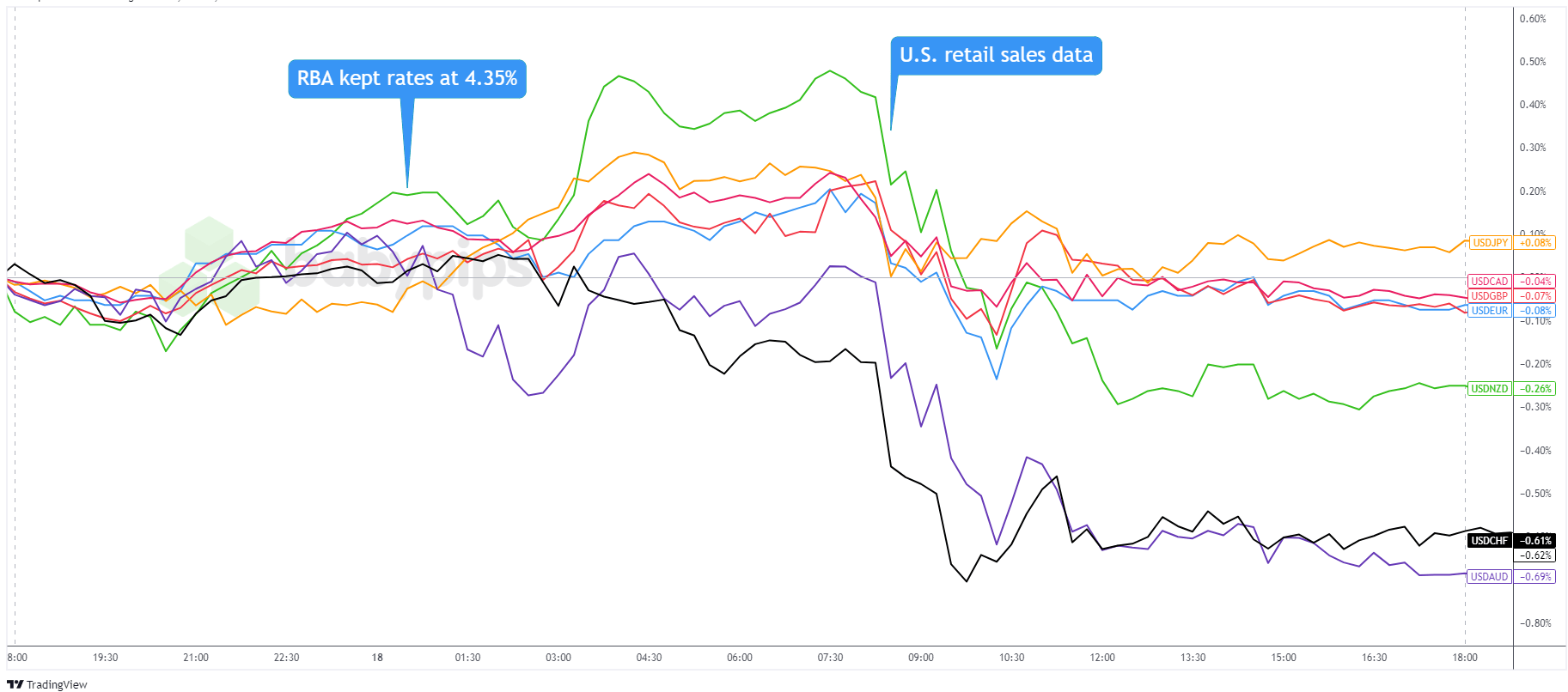

Overlay of USD vs. Major Currencies Chart by TradingView

The U.S. dollar kicked off the day showing some resilience, except against the Australian dollar, which was buoyed by a “hawkish hold” event from the RBA.

Dollar demand remained stable during the European trading session but faltered after a U.S. retail sales report came in weaker than expected. This dip occurred despite a positive industrial production report AND some FOMC members repeating their hawkish biases!

The dollar traded in tight ranges for the rest of the day, likely due to a lack of fresh catalysts and U.S. traders leaving their desks early ahead of the Juneteenth bank holiday.

Upcoming Potential Catalysts on the Economic Calendar:

- U.K.’s CPI and PPI reports at 6:00 am GMT

- Euro Area current account at 8:00 am GMT

- U.K.’s house price index at 8:30 am GMT

- U.S. NAHB housing market index at 2:00 pm GMT

- U.S. markets out on bank holiday

- New Zealand’s quarterly GDP at 10:45 pm GMT

With the U.S. markets out on bank holiday, the markets’ focus may be on the European data releases. The U.K. CPI and PPI reports, in particular, may see increased scrutiny ahead of this week’s Bank of England (BOE) policy decision.

Looking for your own spot to record your market observations & trading statistics? If so, then check out TRADEZELLA! It’s an easy-to-use

journaling tool that can lead to valuable performance & strategy insights! You can easily add your thoughts, charts & track your psychology with each and every trade. Click here to see if it’s right for you!Disclaimer: Babypips.com earns a commission from any signups through our affiliate link. When you subscribe to a service using our affiliate links, this helps us to maintain and improve our content, a lot of which is free and accessible to everyone–including the School of Pipsology! We appreciate your support and hope that you find our content and services helpful. Thank you!