It was a volatile day for most asset classes, as Treasury yields and bitcoin tumbled while commodities and equities had quite the comeback later on.

Still, the safe-haven U.S. dollar was able to keep its head afloat, despite some risk-on flows towards the latter part of the New York session.

Read on to find out which catalysts drove the financial markets earlier:

Headlines:

- Major Chinese state-owned banks sold USD/CNY in coordinated yuan intervention, following the currency’s tumble to its weakest level since Nov 2023

- Australia’s NAB business confidence index in May: -3 (previous reading upgraded from +1 to +2)

- Japanese preliminary machine tool orders rebounded 4.2% y/y in May from earlier 8.9% drop

- U.K. claimant count change in May: 50.4K (10.2K forecast, 8.4K previous)

- U.K. unemployment rate rose from 4.3% to 4.4% versus expectations of no change

- U.K. average earnings index in three-month period ending in April: 5.9% 3m/y (5.7% forecast, previous reading upgraded from 5.7% to 5.9%)

- U.S. NFIB Small Business Index in May: 90.5 (89.8 expected, 89.7 previous)

- EIA raised world oil demand forecast for 2024 and 2025

- World Bank raised 2024 global GDP growth forecast to 2.6% from 2.4%

- Canada’s building permits in April: 20.5% m/m (4.9% expected, -12.3% previous)

- U.S. Treasury auction yielded strong demand for 10-year notes at a high yield of 4.438%

- New Zealand visitor arrivals slumped 9.4% m/m in April, previous reading upgraded from 9.1% to 9.7%

- Japan’s producer price index in May: 2.4% y/y (2.0% expected, previous reading upgraded from 0.9% to 1.1%)

Broad Market Price Action:

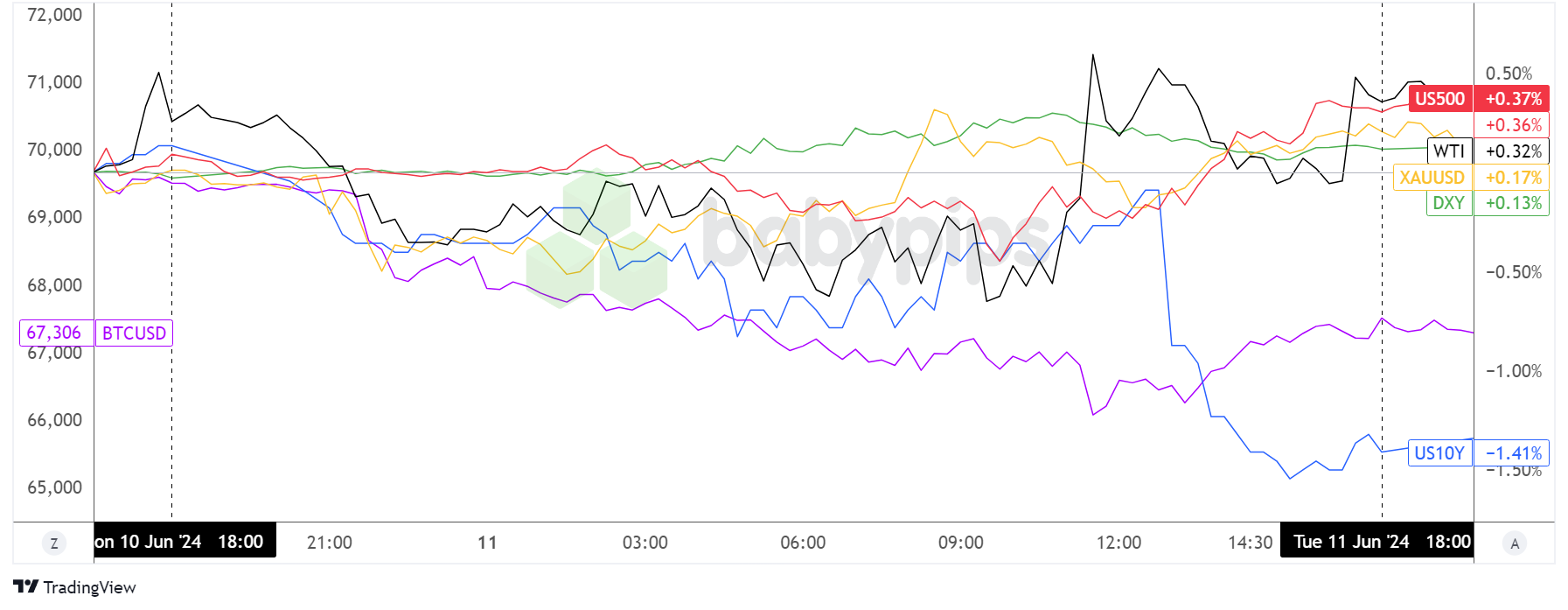

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Market volatility was already in play for bitcoin, gold, and crude oil early on, as these risk assets took hits during the Asian trading session before levelling off towards the London market hours.

U.S. bond yields also cruised lower and moved sideways, then a sharp tumble ensued right around the Treasury auction which yielded a $39 billion sale in 10-year notes, with strong investor demand suggesting that they were willing to settle for lower yields.

WTI crude oil managed to pull higher during the New York session, thanks to the EIA’s positive revision to global oil demand forecasts for this year and the next. Risk-taking also likely got a boost from the World Bank’s increase in global GDP forecast from 2.4% to 2.6% this 2024.

FX Market Behavior: U.S. Dollar vs. Majors

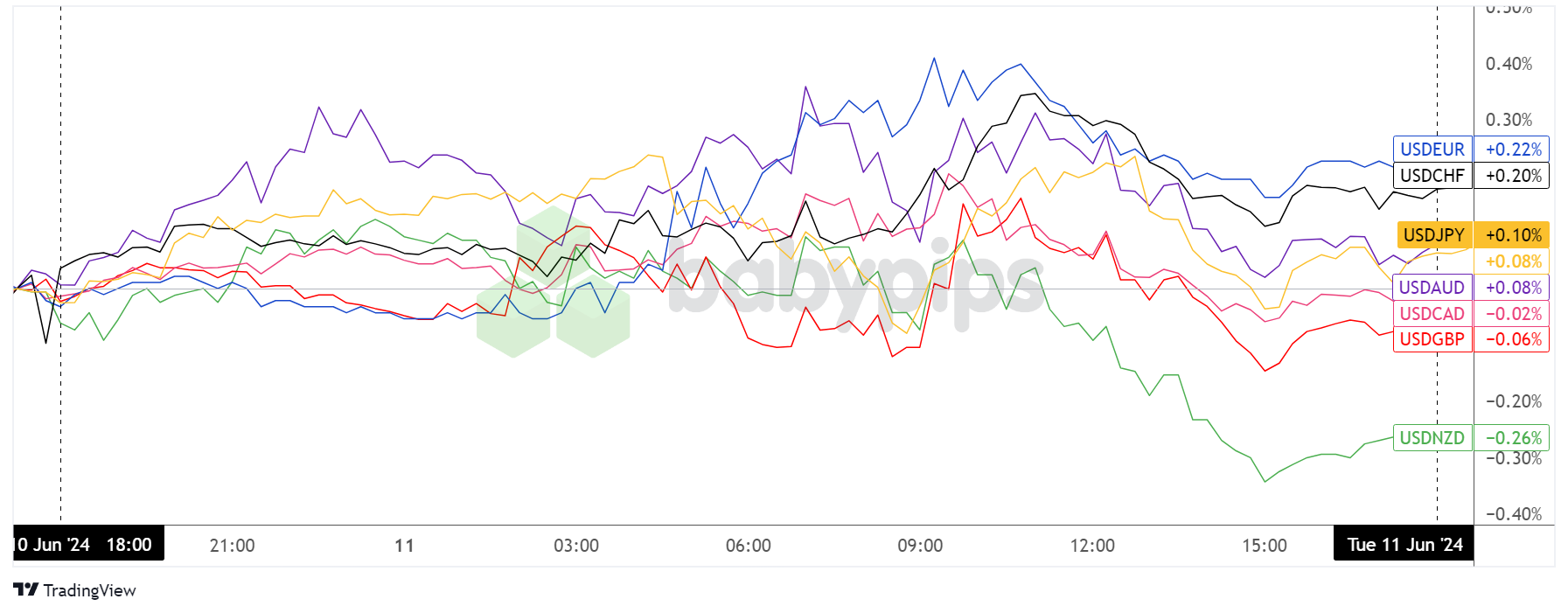

Overlay of USD vs. Major Currencies Chart by TradingView

Major pairs were off to a mixed start, as the U.S. dollar advanced strongly against the Aussie while giving up some ground against the euro and pound early on. News of yuan intervention among China’s state banks likely put AUD on shaky footing, along with the downtick in the Land Down Under’s NAB business confidence index.

From there, the dollar still struggled to establish a clear direction against its peers since data was light and traders were likely playing it safe ahead of the U.S. CPI release and FOMC statement today.

Sterling took some hits during the release of a mixed U.K. jobs report but eventually pared these losses to end up slightly higher versus the dollar while the euro remained on weak footing due to political uncertainty from France’s snap election.

Upcoming Potential Catalysts on the Economic Calendar:

- U.K. monthly GDP at 6:00 am GMT

- U.K. goods trade balance and industrial production at 6:00 am GMT

- U.S. headline and core CPI at 12:30 pm GMT

- U.S. EIA crude oil inventories at 2:30 pm GMT

- FOMC monetary policy statement at 6:00 pm GMT

- FOMC economic projections at 6:00 pm GMT

- FOMC press conference at 6:30 pm GMT

- BOC Governor Macklem’s testimony at 7:15 pm GMT

All eyes and ears are on the U.S. CPI report and FOMC decision today, as market players are likely to examine every detail of the inflation figures to gauge its potential impact on the Fed’s announcement and outlook for borrowing costs.

Don’t forget to look at the updated Fed growth and inflation estimates, as well as the dot plot forecasts for interest rates, as these would likely shape USD trends!

Looking for your own spot to record your market observations & trading statistics? If so, then check out TRADEZELLA! It’s an easy-to-use

journaling tool that can lead to valuable performance & strategy insights! You can easily add your thoughts, charts & track your psychology with each and every trade. Click here to see if it’s right for you!Disclaimer: Babypips.com earns a commission from any signups through our affiliate link. When you subscribe to a service using our affiliate links, this helps us to maintain and improve our content, a lot of which is free and accessible to everyone–including the School of Pipsology! We appreciate your support and hope that you find our content and services helpful. Thank you!