“Risk” assets and usual U.S. dollar counterparts saw gains during the U.S. session as more traders priced in a potential interest rate cut by the Fed.

The U.S. dollar itself was pretty stable, as it gave up pips to commodity-related currencies but also registering gains against fellow safe havens like JPY and CHF.

Headlines:

- Australia’s GDP grew by 0.1% q/q in Q1 2024 vs. 0.3% expected, 0.2% previous

- China Caixin services PMI for May: 54.0 vs. 52.5 forecast and previous; Firms raised their charges amid rising cost burdens; Staffing levels expanded for the first time in four months

- HCOB France final services PMI revised lower from 49.4 to 49.3 in May vs. 49.4 forecast; Job creation cooled slightly; The rate of inflation was at its weakest since July 2021

- HCOB Germany final services PMI revised higher from 52.9 to 54.2 vs. 53.9 forecast; Job creation accelerated to the quickest since June; There were less substantial price increases for end consumers

- HCOB Eurozone final services PMI revised lower from 53.3 to 53.2 in May vs. 53.3 forecast; Job creation matched April’s fastest since June 2023; The rate of inflation in selling charges eased to a six-month low

- S&P Global UK final services PMI kept at 52.9 as expected in May; Prices rose at the slowest pace for over three years; Job creation accelerated to the quickest since February

- Euro Area producer prices for April: -1.0% m/m vs. -0.6% forecast, -0.5% previous

- U.S. ADP non-farm employment change showed 152K net job additions in May vs. 173K forecast and 183K increase in April

- BOC cut its rates by 25bps to 4.75% as expected in June and hinted at future rate cuts

- S&P Global US final services PMI maintained at 54.8 as expected in May; Service providers continued to lower their staffing levels in May; There was a faster increase in selling prices

- U.S. ISM services PMI for May: 53.8 vs. 51.0 forecast, 49.4 previous; Employment grew from 45.9 to 47.1; the Prices index slipped from 59.2 to 58.1

- EIA: U.S. crude oil inventories increased by 1.2M barrels in the week ending May 31 vs. 2.1M barrel draw expected, 4.2M barrel decrease in the previous week

Broad Market Price Action:

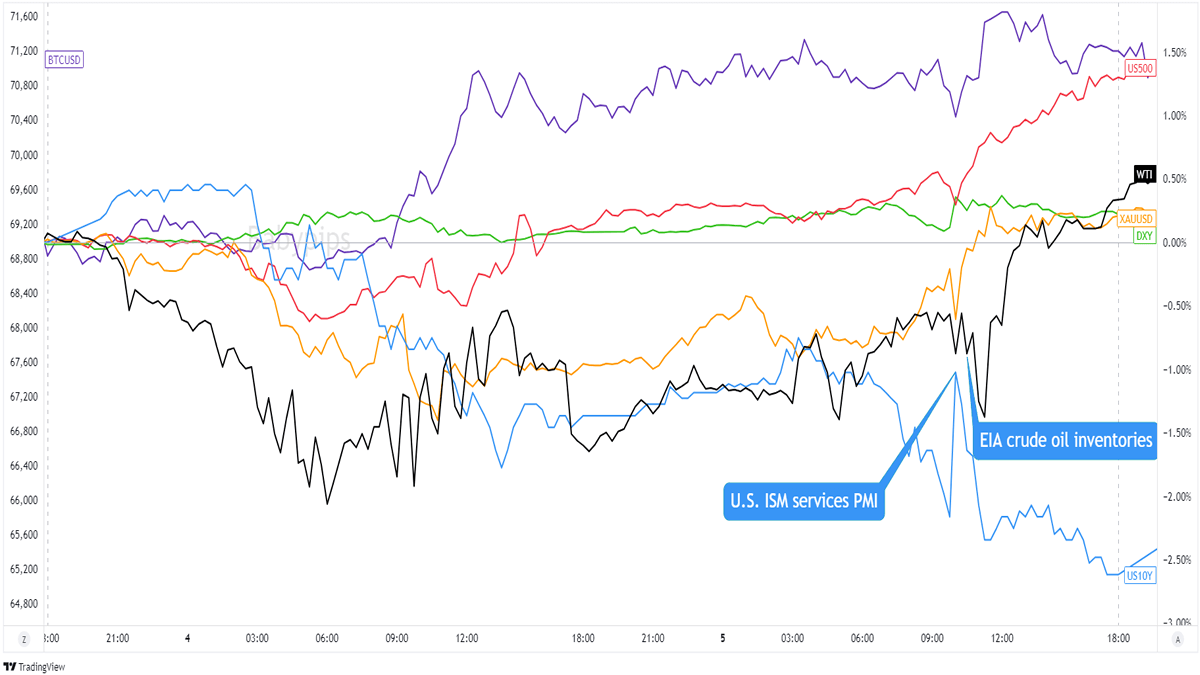

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

The major financial assets were all over the place today, with crude oil and spot gold losing ground during the Asian session on overall risk appetite and a bit of stability for the U.S. dollar.

The tides turned a few hours after the European session open as mixed (but mostly positive) Euro Area PMIs and ECB rate cut bets encouraged risk-taking. Bitcoin (BTC/USD), oil, and the S&P 500 futures traded higher while the U.S. 10-year yields and spot gold turned lower.

A U.S. ADP report miss during the U.S. session piled on to this week’s disappointing JOLTS jobs data and U.S. S&P manufacturing PMI and amped up the market’s bets for a Fed rate cut. ISM’s manufacturing PMI showed strength but also noted a weakness in the employment component.

It didn’t help that the BOC cut its interest rates – the first G7 central bank to do so in years – and highlighted the increased odds of rate cuts by other central banks.

The pro-rate cut environment dragged the U.S. 10-year yields below 4.30% and boosted USD counterparts like crude oil, spot gold, and U.S. equities. The S&P 500 and Nasdaq indicies even clocked in new record highs!

FX Market Behavior: U.S. Dollar vs. Majors

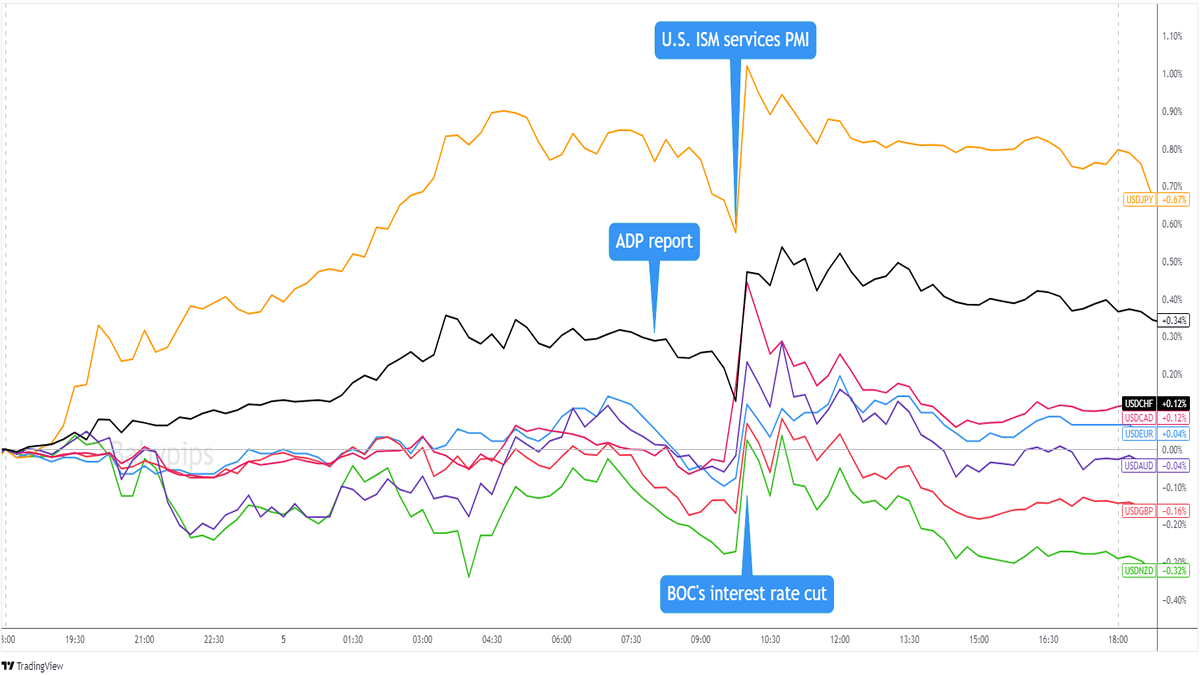

Overlay of USD vs. Major Currencies Chart by TradingView

The U.S. dollar had a relatively chill day, extending its gains against fellow safe havens like the Japanese yen and Swiss franc during the Asian and early European sessions.

The Greenback received a boost following a better-than-expected ISM services PMI release, but the move was quickly reversed as traders focused on the persistently weak employment component.

The BOC also cut its interest rates, which brought a risk-friendly trading environment that dragged the safe haven USD lower.

The dollar ended the day not too far from its daily open prices, with gains against JPY, CHF, CAD, and EUR but also losses against “riskier” bets like AUD, NZD, and GBP.

Upcoming Potential Catalysts on the Economic Calendar:

- Switzerland’s unemployment rate at 5:45 am GMT

- Germany’s factory orders at 6:00 am GMT

- Italy’s retail sales at 8:00 am GMT

- U.K.’s construction PMI at 8:30 am GMT

- Euro Area retail sales at 9:00 am GMT

- U.S. Challenger job cuts at 11:30 am GMT

- ECB’s policy decision at 12:15 pm GMT, presser at 12:45 pm GMT

- U.S. initial jobless claims at 12:30 pm GMT

- Canada’s trade balance at 12:30 pm GMT

- U.S. revised non-farm productivity and labor costs at 12:30 pm GMT

- U.S. trade balance at 12:30 pm GMT

- Canada’s IVEY PMI at 2:00 pm GMT

- New Zealand’s manufacturing sales at 10:45 pm GMT

- Japan’s household spending at 11:30 pm GMT

The European Central Bank (ECB) is expected to follow BOC in cutting its interest rates this month. But, according to our Event Guide for ECB’s decision, the presser that would follow may gain more attention from the markets.

Meanwhile, the Challenger job cuts and initial jobless claims data from the U.S. may move the needle for the dollar and its usual counterparts as traders reprice their Fed rate cut bets.

Looking for your own spot to record your market observations & trading statistics? If so, then check out TRADEZELLA! It’s an easy-to-use

journaling tool that can lead to valuable performance & strategy insights! You can easily add your thoughts, charts & track your psychology with each and every trade. Click here to see if it’s right for you!Disclaimer: Babypips.com earns a commission from any signups through our affiliate link. When you subscribe to a service using our affiliate links, this helps us to maintain and improve our content, a lot of which is free and accessible to everyone–including the School of Pipsology! We appreciate your support and hope that you find our content and services helpful. Thank you!