Revised U.S. economic growth data sent the U.S. dollar and other major financial assets all over the charts yesterday!

What exactly did market players need to price in?

We have a list of yesterday’s top headlines:

Headlines:

- FOMC voting member Raphael Bostic expects the Fed to be prepared to cut interest rates near the end of the year in Q4 2024

- SNB Chairman Thomas Jordan said there’s a “small upward risk to the inflation forecasts” associated with a weaker Swiss franc

- Australia’s capital expenditure rose by another 1.0% q/q in Q1 2024 after a 0.9% gain in Q4 2023 (0.6% expected)

- New Zealand’s 2024 budget statement sees interest rates “gradually easing from late 2024” and projects a return to a budget surplus by 2027 – 2028, a year later than previously expected

- Switzerland’s economy – adjusted for large sports events – grew 0.5% q/q in Q1 2024 (vs. 0.3% expected and previous) and marked the fastest growth since Q2 2022

- Euro Area unemployment rate slipped from 6.5% to 6.4% (vs. 6.5% expected) in April

- The second (preliminary) reading of the U.S. GDP showed a revision from 1.6% q/q to 1.3% q/q (vs. 1.2% expected) in Q1 2024; Price index slowed from 3.1% q/q to 3.0% q/q (vs. 3.1% expected)

- U.S. initial jobless claims rose from 216K to 219K (vs. 218K expected) in the week ending May 25

- U.S. goods trade deficit widened from $92.3B to $99.4B – the widest since May 2022 – in April as imports (3.1% m/m) outpaced exports (0.5% m/m)

- U.S. pending home sales fell by 7.7% m/m in April – the slowest pace since April 2020 – vs. 1.1% dip expected, 3.6% gain in March

- EIA crude oil inventories showed a 4.2M barrel draw in the week ending May 24 (vs. -1.6M expected, 1.8M previous)

- FOMC voting member John Williams said the Fed has “the time and ability” to collect more data while the U.S. is on a “reasonably good track” to taming inflation without an economic downturn

- Tokyo’s core CPI for May: 1.9% m/m as expected (vs. 1.6% previous)

Broad Market Price Action:

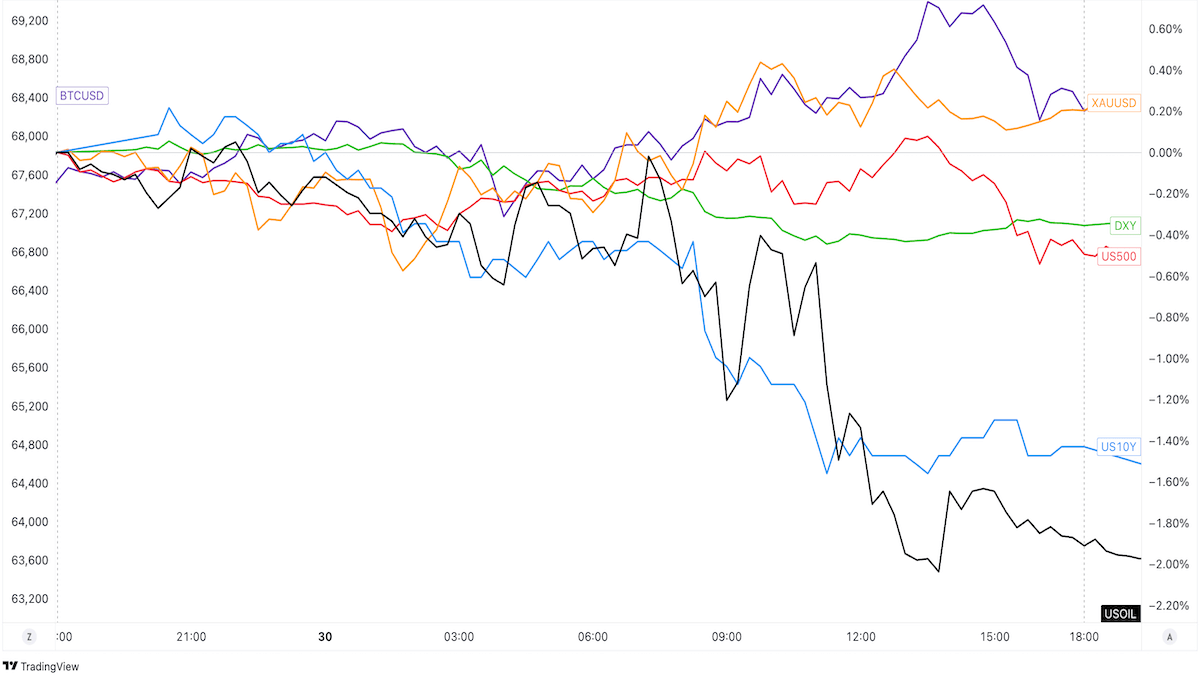

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Volatility was relatively tight during the Asian session trading even as the major assets lowkey extended their price action from Wednesday’s U.S. session trading.

Gold and crude oil traded lower as traders priced in a “higher for longer” interest rate environment in the U.S. and its impact on global demand, while U.S. 10-year Treasury yields extended its bearish pullback from its 4.63% intraweek highs.

Fortunately for gold bugs, spot gold turned bullish at the start of the European session when traders first stayed away from “risky” bets ahead of the U.S. data releases and then again during the U.S. session when it served as a counterpart to a weak U.S. dollar. Bitcoin (BTC/USD) was also a winner, finding support from its 67,150 weekly lows to hit the $68,400 area before pulling back down.

The release of weaker-than-expected mid-tier reports from the U.S. cast doubt on the resilience of Uncle Sam’s growth and encouraged growth concerns and interest rate cut bets at the same time.

U.S. oil prices dropped sharply on demand concerns while U.S. 10-year yields extended its decline and the U.S. dollar index capped the day in the red.

FX Market Behavior: U.S. Dollar vs. Majors

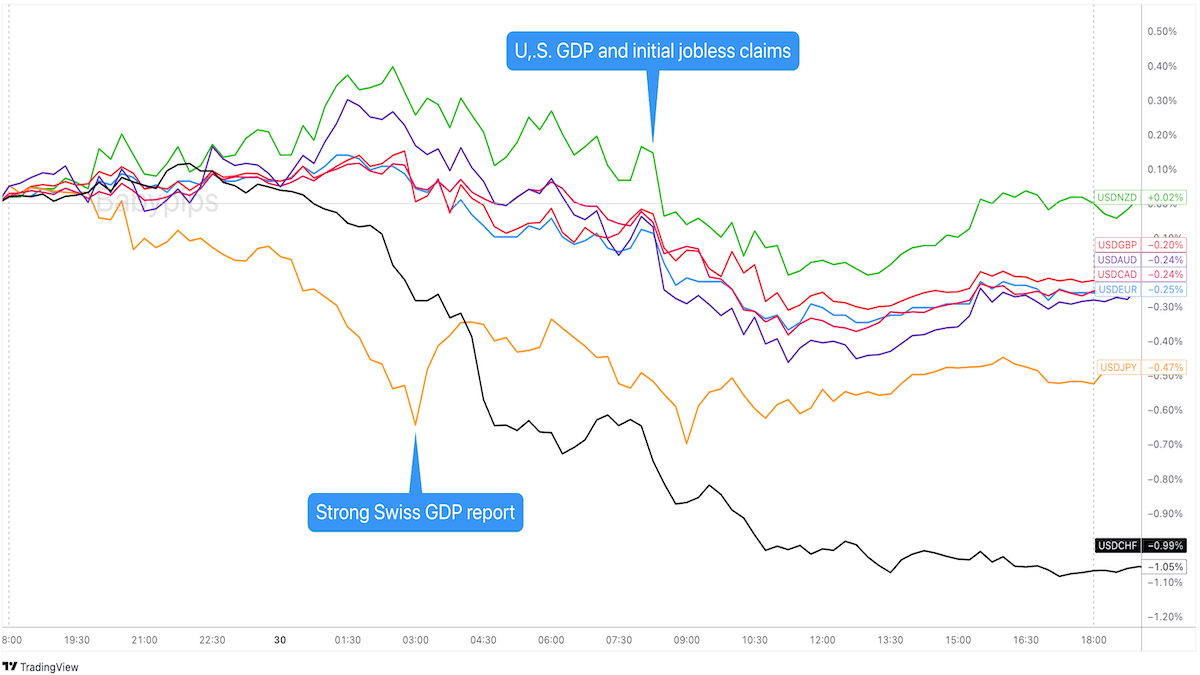

Overlay of USD vs. Major Currencies Chart by TradingView

The U.S. dollar started losing ground during the late Asian and early European session as traders started taking off their USD-bullish bets ahead of Thursday’s U.S. data releases.

Downward revisions to the Q1 2024 GDP and GDP price indices, as well as weaker-than-expected figures from the initial jobless claims data and pending home sales accelerated the dollar’s losses during the U.S. session.

The Greenback eventually traded in ranges and even saw minimal pullbacks before ending the day lower against its major counterparts. The dollar is weakest against the Swiss franc following a better-than-expected Swiss GDP release, while it’s seeing minimal losses against “risky” bets like NZD, GBP, and AUD.

Upcoming Potential Catalysts on the Economic Calendar:

- China’s manufacturing and services PMIs at 1:30 am GMT

- Japan’s housing starts at 5:00 am GMT

- Germany’s retail sales at 6:00 am GMT

- U.K.’s Nationwide house price index at 6:30 am GMT

- France’s preliminary CPI and GDP at 6:45 am GMT

- U.K.’s mortgage approvals at 8:30 am GMT

- Euro Area CPI flash estimate at 9:00 am GMT

- Canada’s monthly GDP at 12:30 pm GMT

- U.S. core PCE price index at 12:30 pm GMT

- U.S. Chicago PMI at 1:45 pm GMT

The markets’ attention may shift to the Euro Area today with inflation updates from the region and Germany’s retail sales data scheduled for release.

Then again, volatility may be limited ahead of the anticipated U.S. core PCE price index report, which is expected to keep its monthly reading but also show a slight downward revision to the annual figure.

Looking for your own spot to record your market observations & trading statistics? If so, then check out TRADEZELLA! It’s an easy-to-use

journaling tool that can lead to valuable performance & strategy insights! You can easily add your thoughts, charts & track your psychology with each and every trade. Click here to see if it’s right for you!Disclaimer: Babypips.com earns a commission from any signups through our affiliate link. When you subscribe to a service using our affiliate links, this helps us to maintain and improve our content, a lot of which is free and accessible to everyone–including the School of Pipsology! We appreciate your support and hope that you find our content and services helpful. Thank you!