The Greenback was a big winner in the latest trading sessions, thanks to rising bond yields and some risk-off flows.

Not even a somewhat somber Fed Beige Book seemed enough to stop the dollar’s climb, as inflation and jobs indicators still printed modest improvements.

Check out the rest of the market headlines to see what went down:

Headlines:

- Australia’s MI leading index for April: 0.0% (-0.1% previous)

- ANZ business confidence index for May: 11.2 (14.9 previous)

- Australian CPI for April: 3.6% y/y (3.4% expected, 3.5% previous)

- Australian construction work done for Q1: -2.9% q/q (+0.6% expected, 1.8% previous)

- Japanese consumer confidence index for May: 36.2 (39.1 expected, 38.3 previous)

- German GfK consumer climate index for May: -20.9 (-22.5 expected, previous reading upgraded from -24.2 to -24.0)

- German preliminary CPI for May: 0.1% m/m (0.2% expected, 0.5% previous)

- Swiss UBS economic expectations index for April: 18.2 (17.6 previous)

- U.S. Richmond manufacturing index for May: 0 (-6 expected, -7 previous)

- Fed Beige Book: National economic activity expanded but varied across districts, “lower discretionary spending” due to price sensitivity, job gains “negligible”

- New Zealand building consents in April: -1.9% m/m (-0.2% previous)

Broad Market Price Action:

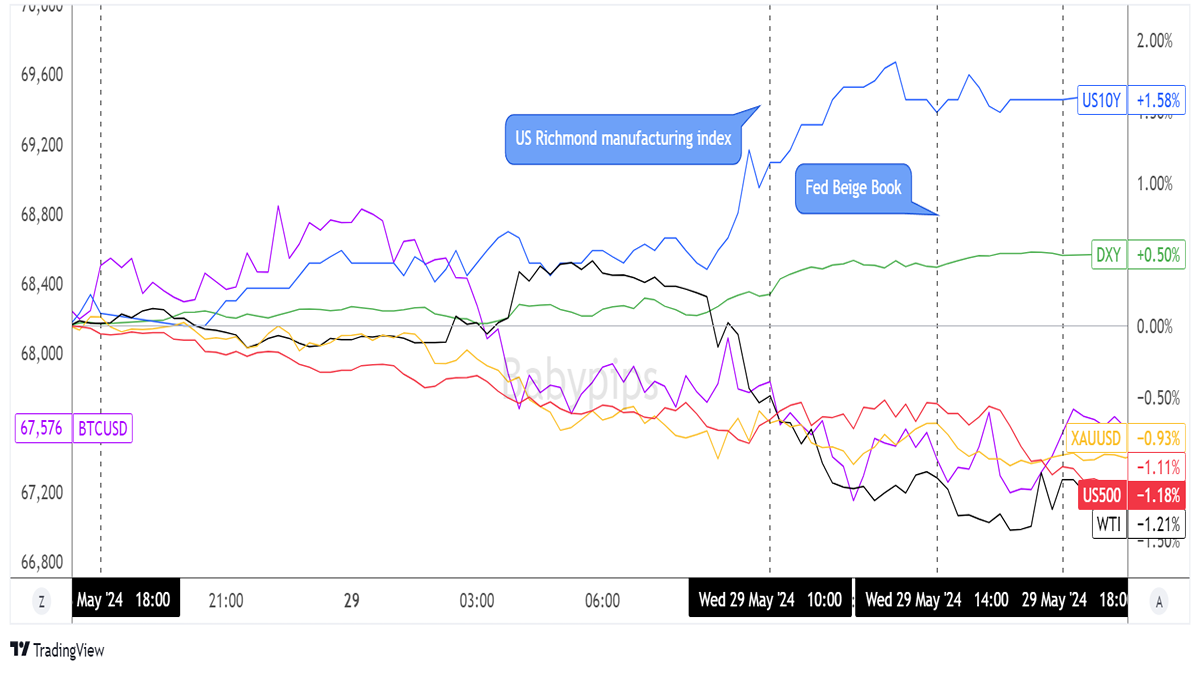

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Risk-off vibes were present as early as Wednesday’s Asian trading session, as market players continued to monitor geopolitical tensions in the Middle East. The S&P 500 index crawled lower, along with gold and crude oil, while the safe-haven dollar and bond yields chalked up a few gains.

Oil recovered slightly during the London trading session thanks to reports that the OPEC+ might decide to keep output cuts in place for a bit longer due to rising global inventory levels. However, the energy commodity soon joined the rest of the risk assets in a slump, as the dollar and Treasury yields surged.

FX Market Behavior: U.S. Dollar vs. Majors

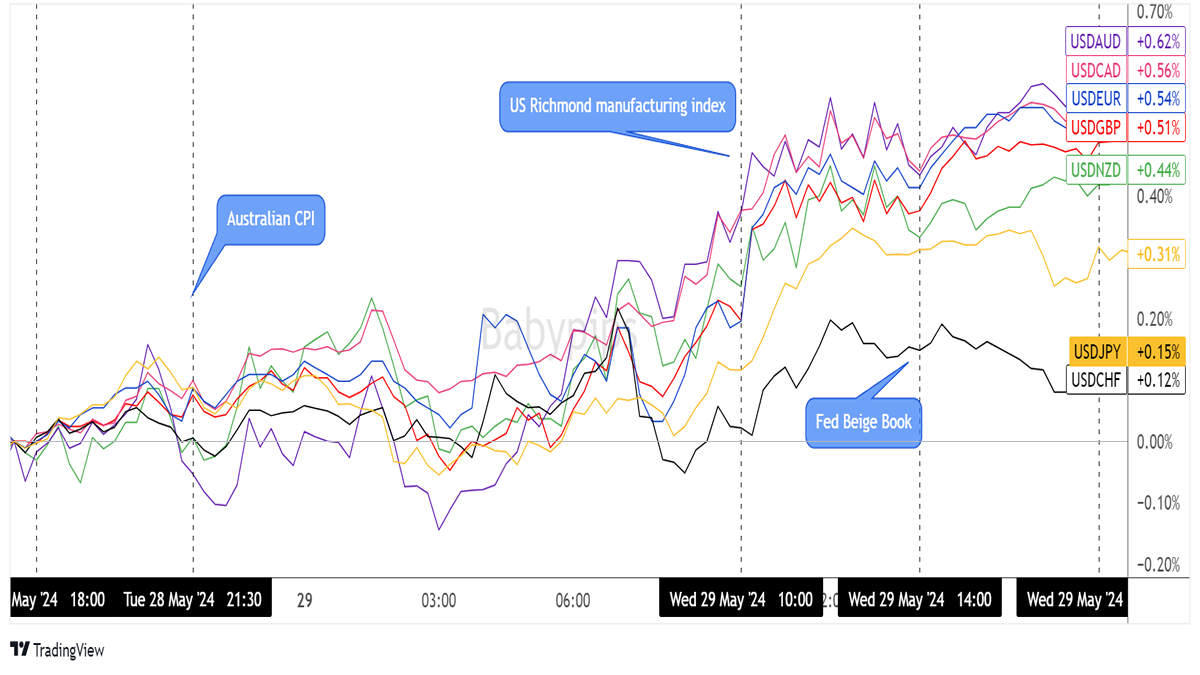

Overlay of USD vs. Major Currencies Chart by TradingView

The safe-haven dollar continued to take advantage of risk aversion stemming from geopolitical tensions, advancing across the board before giving up a bit of ground to AUD ahead of the Australian CPI release.

The actual figure came in better than expected at 3.6% year-on-year versus the projected decline from 3.5% to 3.4%. This allowed the Aussie to put up a pretty decent fight against the U.S. dollar until risk-off flows kicked into high gear later in the day, leaving AUD to end 0.62% lower against USD.

Stronger than expected Richmond manufacturing survey data lifted the Greenback further, as the reading turned out flat in May instead of the estimated -6 figure. However, the dollar pared some of its gains when the Fed Beige Book indicated a lackluster assessment of the economy, with majority of Fed districts reporting marginal job gains and subdued consumer spending due to higher prices.

Other lower-yielding currencies namely JPY and CHF managed to minimize losses against the U.S. dollar while the oil-related Loonie trailed weaker commodity prices to end up more than 0.5% in the red.

Upcoming Potential Catalysts on the Economic Calendar:

- Swiss GDP at 7:00 am GMT

- Swiss KOF economic barometer at 7:00 am GMT

- Spanish flash CPI at 7:00 am GMT

- U.S. preliminary GDP at 12:30 pm GMT

- U.S. weekly initial jobless claims at 12:30 pm GMT

- U.S. pending home sales at 2:00 pm GMT

- U.S. EIA crude oil inventories at 3:00 pm GMT

- Tokyo core CPI at 11:30 pm GMT

- Japanese jobless rate at 11:30 pm GMT

- Japanese preliminary industrial production at 11:50 pm GMT

- Japanese retail sales at 11:50 pm GMT

It’s bound to be another eventful day for the U.S. dollar, as Uncle Sam gears up to release the second version of its Q1 2024 growth figure. Downward revisions are eyed, which might impact Fed policy expectations and overall market sentiment, so make sure you check out our Event Guide for the U.S. preliminary GDP.

Don’t forget that the weekly initial jobless claims report due at the same time tends to spur strong intraday USD volatility, too!

Looking for your own spot to record your market observations & trading statistics? If so, then check out TRADEZELLA! It’s an easy-to-use

journaling tool that can lead to valuable performance & strategy insights! You can easily add your thoughts, charts & track your psychology with each and every trade. Click here to see if it’s right for you!Disclaimer: Babypips.com earns a commission from any signups through our affiliate link. When you subscribe to a service using our affiliate links, this helps us to maintain and improve our content, a lot of which is free and accessible to everyone–including the School of Pipsology! We appreciate your support and hope that you find our content and services helpful. Thank you!