FX volatility is heating up with the release of top-tier economic reports from the major economies!

Meanwhile, the Fed’s May meeting minutes supported a “higher for longer” interest rate environment in the U.S. and boosted the U.S. dollar against some of its usual asset counterparts.

We have the details on today’s biggest market movers!

Headlines:

- RBNZ delivered a “hawkish hold” with interest rate hike talks and higher inflation projections

- U.K.’s annual CPI dropped from 3.2% y/y to a three-year low of 2.3% y/y in April (vs 2.1% forecast); Core CPI eased from 4.2% y/y to 3.9% y/y (vs. 3.6% forecast)

- U.K.’s PPI input for April: 0.6% m/m (3.6% expected, -0.2% previous); PPI output at 0.2% (0.4% expected, 0.2% previous)

- Germany’s Bundesbank said GDP is “likely to increase slightly again” in Q2 2024 following a 0.2% uptick in Q1

- U.S. existing home sales for April is 1.9% lower at 4.14M (vs. 4.21M expected, 4.22M previous)

- EIA’s U.S. crude oil inventories increased by 1.8M barrels in the week ending May 17 (vs. -2.4M expected, -2.5M previous)

- FOMC’s May meeting minutes highlighted the members’ concerns over persistently high inflation

- RBNZ Gov. Orr downplayed rate hike expectations, saying it would only be “meaningful” if inflation expectations rise uncontrollably due to actual inflation

- New Zealand retail sales for Q1 2024: 0.5% q/q (-0.3% expected, -1.8% previous); Core retail sales rise by 0.4% q/q (0.0% expected, -1.6% previous)

- Australia’s Judo Bank flash manufacturing PMI jumped from 48.6 to an eight-month high of 48.9; Services PMI dropped from 53.1 to a three-month low of 53.6 in May

Broad Market Price Action:

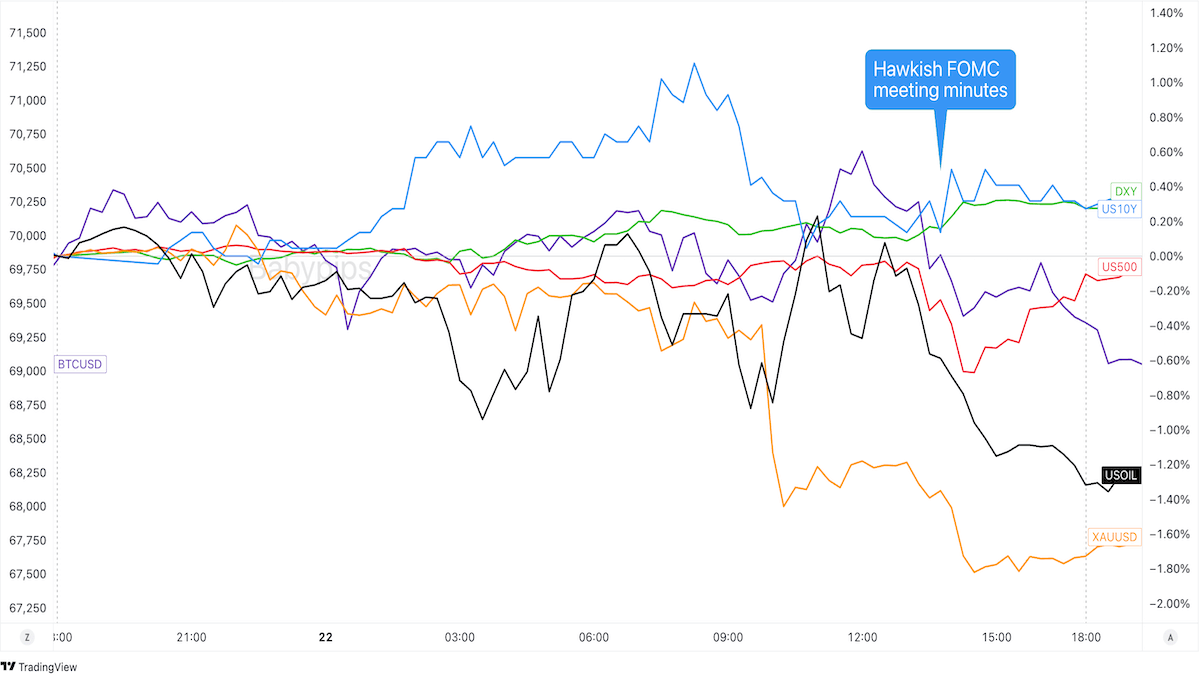

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

The major financial assets traded in ranges during the Asian session as traders waited for top-tier economic data due later in the day.

One highlight was the RBNZ’s decision to keep its interest rates steady at 5.50% but also up its “peak” interest rate bets and delay its first rate cut projections.

Volatility started firing up at the start of London session trading when the U.S. 10-year bond yields rose and crude oil prices took hits likely in anticipation of a potentially hawkish FOMC meeting minutes.

A hot U.K. CPI report may have also helped push government bond yields higher as trader pared back their BOE rate cut bets.

The tides briefly turned at the release of weaker-than-expected U.S. existing home sales data. Luckily for USD bulls, a hawkish FOMC meeting minutes soon bumped U.S. bond yields and the U.S. dollar higher while weighing on counterparts like spot gold, crude oil, bitcoin, and U.S. equities.

FX Market Behavior: U.S. Dollar vs. Majors

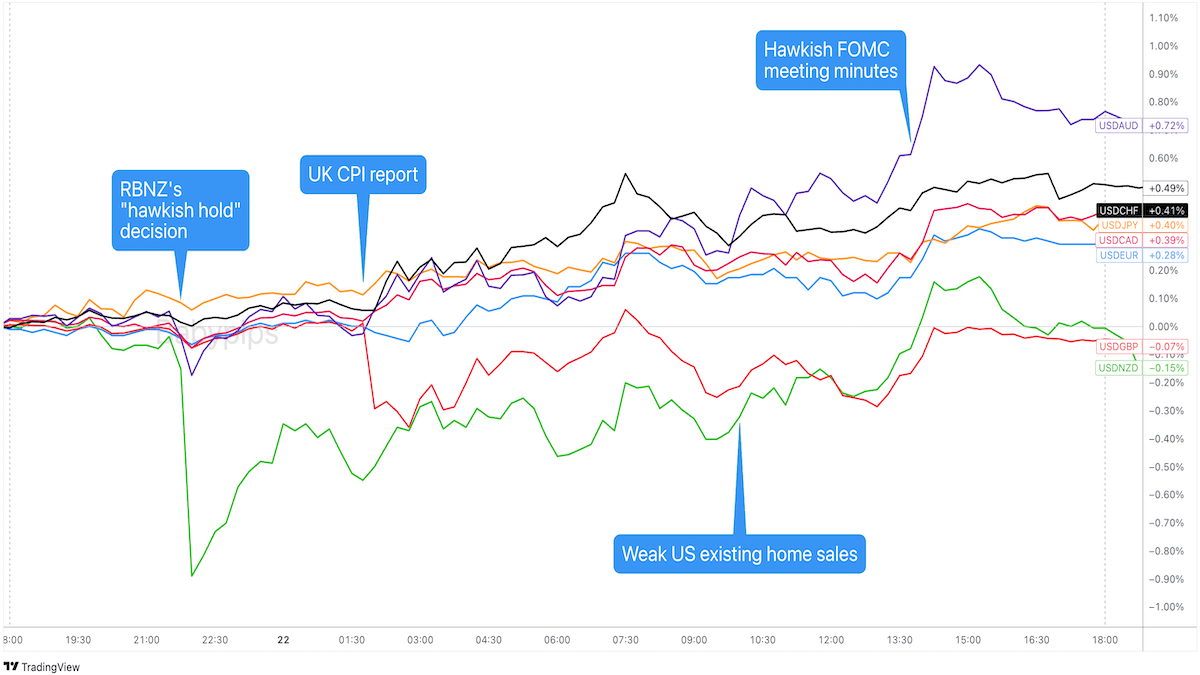

Overlay of USD vs. Major Currencies Chart by TradingView

It was a busy day for dollar traders, who priced in the RBNZ’s “hawkish hold” decision during the Asian session and the U.K.’s hot inflation report during the London session.

Price action took an even livelier turn when the Fed’s May meeting minutes showed FOMC members anticipating that it would take them longer than previously expected to be confident that inflation is decelerating enough to hit their 2% target.

Not even the dollar’s strength was able to propel USD in the green against intraday winners like GBP and NZD but the Greenback managed to maintain its gains against its other major counterparts.

Upcoming Potential Catalysts on the Economic Calendar:

- France’s flash manufacturing and services PMIs at 7:15 am GMT

- Germany’s flash manufacturing and services PMIs at 7:30 am GMT

- Euro Area’s flash manufacturing and services PMIs at 8:00 am GMT

- U.K.’s flash manufacturing and services PMIs at 8:30 am GMT

- U.S. initial jobless claims at 12:30 pm GMT

- China’s CB leading index at 1:00 pm GMT

- U.S. flash manufacturing and services PMIs at 1:45 pm GMT

- U.S. new home sales at 2:00 pm GMT

- FOMC voting member Raphael Bostic to give a speech at 7:00 pm GMT

- New Zealand’s trade balance at 10:45 pm GMT

- Japan’s national core CPI at 11:30 pm GMT

It’s global PMI day today! The first indicators of business activity trends all over the world may impact market risk sentiment or at least their individual currencies. Meanwhile, Japan’s inflation report might move JPY pairs around after days of weaknesses.

Looking for your own spot to record your market observations & trading statistics? If so, then check out TRADEZELLA! It’s an easy-to-use

journaling tool that can lead to valuable performance & strategy insights! You can easily add your thoughts, charts & track your psychology with each and every trade. Click here to see if it’s right for you!Disclaimer: Babypips.com earns a commission from any signups through our affiliate link. When you subscribe to a service using our affiliate links, this helps us to maintain and improve our content, a lot of which is free and accessible to everyone–including the School of Pipsology! We appreciate your support and hope that you find our content and services helpful. Thank you!