The major financial assets saw relatively muted volatility as traders waited for anticipated reports scheduled later this week.

Crude oil was dragged lower on concerns over the impact of “higher for longer” global interest rates while ether (ETH/USD) got a boost from ETF approval optimism.

The major FX currencies were mostly in tight ranges except for the Canadian dollar which saw bearish pressure following a softer-than-expected April CPI release.

Read on to see how your favorite financial assets traded!

Headlines:

- RBA’s May meeting minutes showed members discussed the possibility of a rate hike, but the hurdle to do so remained high.

- Germany’s producer prices in April: 0.2% m/m (0.3% expected, 0.2% previous) on lower energy prices

- ECB President Lagarde is confident “we have inflation under control” and sees a “strong likelihood” of a rate cut on June 6

- Euro Area trade surplus in March: 17.3B EUR (19.9B EUR expected, 16.7B EUR previous)

- API: U.S. crude oil inventories rose by 2.48M barrels in the week ending May 17 (vs. 3.104M barrel draw in the previous week)

- Canada’s monthly CPI for April: 0.5% m/m (0.4% expected, 0.6% previous); Core CPI: 0.2% (vs. 0.4% expected, 0.5% previous); Annual CPI slowed from 2.9% to 2.7% (vs. 2.8% expected); Annual core CPI dipped from 2.0% to 1.6% (vs. 2.0% expected)

- FOMC voting member Raphael Bostic is “not in a hurry to cut rates” and thinks one rate cut in Q4 2024 is appropriate

- FOMC voting member Loretta Mester needs “a few more months of inflation data” to be more confident that it’s coming down

- Japan’s core machinery orders increased by 2.9% m/m in March (vs. -1.8% expected, 7.7% previous)

- Japan’s trade deficit shrank from 0.68T JPY to 0.56T JPY in April as exports (+0.9% m/m) outpaced imports (-0.5% m/m)

Broad Market Price Action:

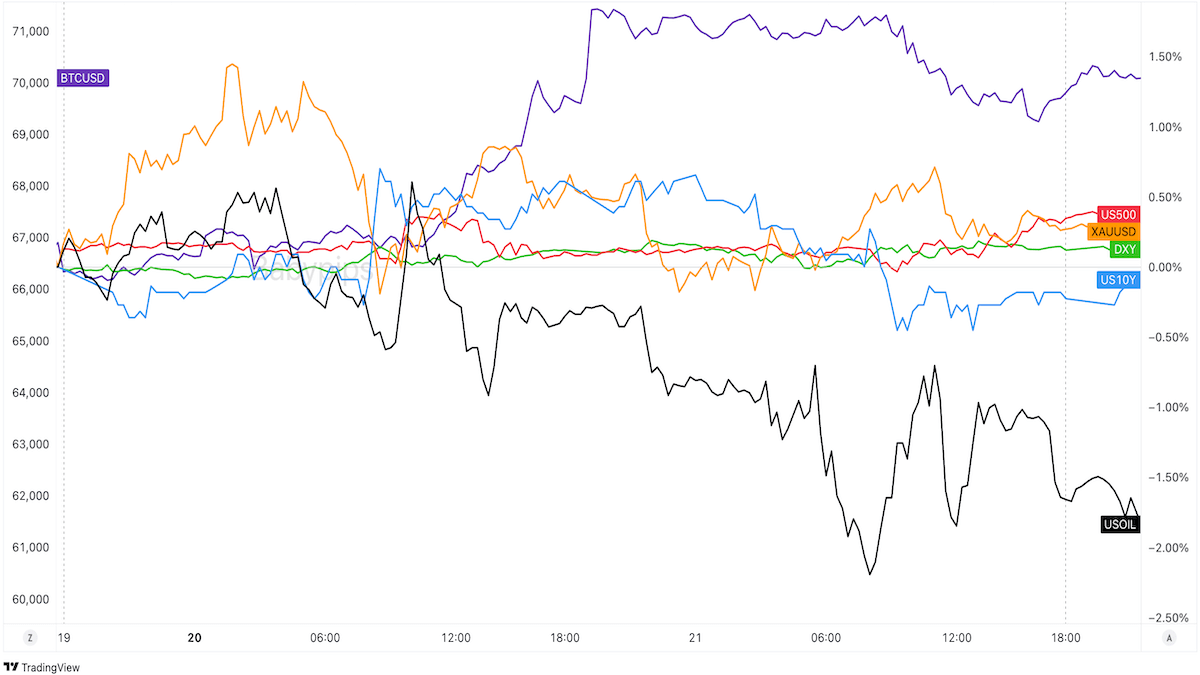

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

The major financial assets once again took cues from individual catalysts while traders likely waited for top-tier reports to lead broader market themes.

Spot gold tried to make another run for the $2,430 area before pulling back to $2,420. U.S. crude oil prices edged lower following a surprise U.S. oil inventory build and over concerns of a “higher for longer” interest rate environment affecting global demand.

Meanwhile, bitcoin (BTC/USD) rose to the $71,000 area likely on traders anticipating a potential spot ETF approval for ether.

The U.S. 10-year bond yields pulled back from its 4.450% levels to trade closer to 4.405% and the U.S. dollar traded in ranges ahead of today’s FOMC meeting minutes release.

FX Market Behavior: U.S. Dollar vs. Majors

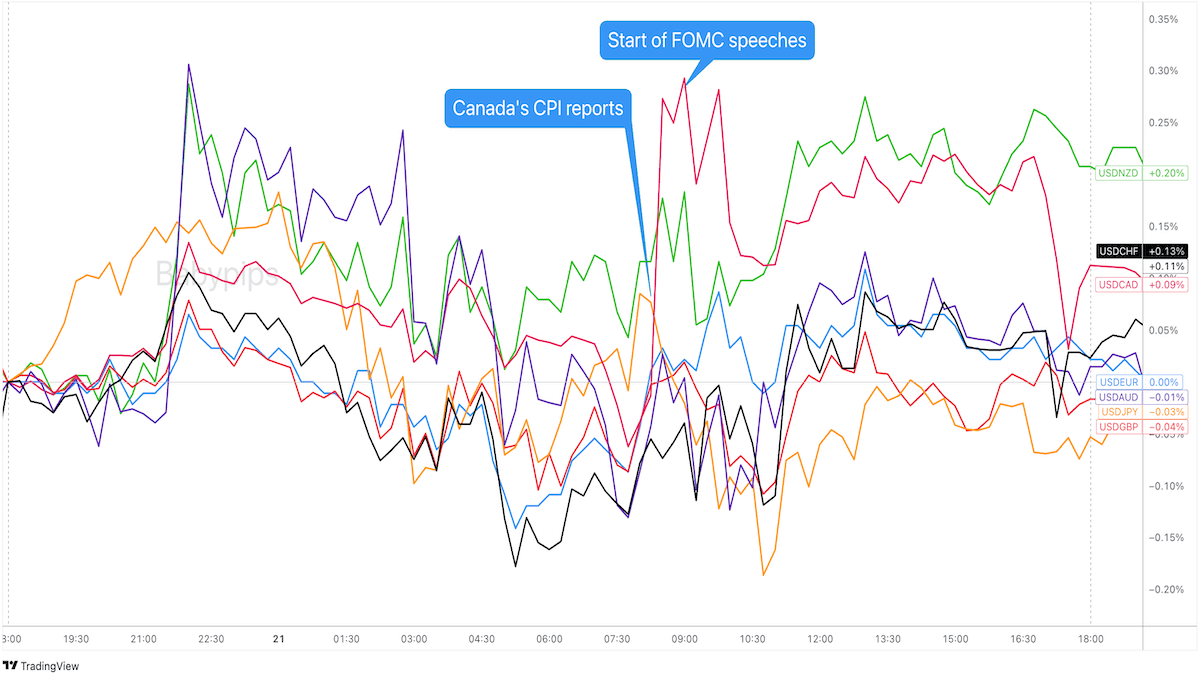

Overlay of USD vs. Major Currencies Chart by TradingView

The U.S. dollar spiked higher at the start of the Asian session before retracing its moves and moving in tight ranges for the rest of the day. While there weren’t direct catalysts for the spike, it’s possible that concerns for China’s economy may have boosted the demand for Asian traders early in the day.

FOMC voting members continued to telegraph their preference to wait a few more months before seriously considering a rate cut but it didn’t help USD demand much in the U.S. session.

Instead, traders are keeping the Greenback in tight(ish) ranges as they wait for anticipated data releases such as the FOMC meeting minutes and U.S. PMI reports.

Upcoming Potential Catalysts on the Economic Calendar:

- U.K.’s CPI and PPI reports at 6:00 am GMT U.K.’s public sector borrowing at 6:00 am GMT

- U.K.’s house price index at 8:30 am GMT

- BOE Deputy Governor Sarah Breeden to participate in a panel discussion at 12:45 pm GMT

- U.S. existing home sales at 2:00 pm GMT

- U.S. crude oil inventories at 2:30 pm GMT

- FOMC meeting minutes at 6:00 pm GMT

- RBNZ Gov. Orr to give a speech at 8:10 pm GMT

- New Zealand’s quarterly retail sales at 10:45 pm GMT

- Australia’s flash manufacturing and services PMIs at 11:00 pm GMT

- Japan’s flash manufacturing PMI at 12:30 am GMT (May 23)

The market plots will thicken in the next trading sessions as we the U.K.’s inflation data and the Fed’s May meeting minutes.

On top of that, PMI reports from Australia and Japan will kick off the business and services sector updates from the major economies. Don’t even think of missing these events!

Looking for your own spot to record your market observations & trading statistics? If so, then check out TRADEZELLA! It’s an easy-to-use

journaling tool that can lead to valuable performance & strategy insights! You can easily add your thoughts, charts & track your psychology with each and every trade. Click here to see if it’s right for you!Disclaimer: Babypips.com earns a commission from any signups through our affiliate link. When you subscribe to a service using our affiliate links, this helps us to maintain and improve our content, a lot of which is free and accessible to everyone–including the School of Pipsology! We appreciate your support and hope that you find our content and services helpful. Thank you!