Markets were off to a bit of a lazy start on Monday, before volatility picked up and led to a mixed run for asset classes.

Crude oil pulled up from an initial slump while gold and Treasury yields edged lower. What’s up with that?!

Headlines:

- New Zealand BusinessNZ services index for April: 47.1 (47.2 previous)

- New Zealand food price index for April: +0.6% m/m (-0.5% previous)

- Australia’s NAB business confidence index for April: 1 (1 previous)

- New Zealand inflation expectations for Q2 2024: 2.33% q/q (2.50% previous)

- Swiss SECO consumer climate index for April: -38 (-40 expected, -38 previous)

- Canada’s building permits for March: -11.7% m/m (-4.6% expected, +8.9% previous)

- FOMC member Jefferson acknowledged progress in inflation reduction and labor market resilience and supported the maintenance of restrictive policy until further evidence of price pressures subsiding

- SNB Chairperson Jordan said that battle against inflation is nearing completion

- Japanese PPI for April: 0.9% y/y (0.9% expected, 0.9% previous)

Broad Market Price Action:

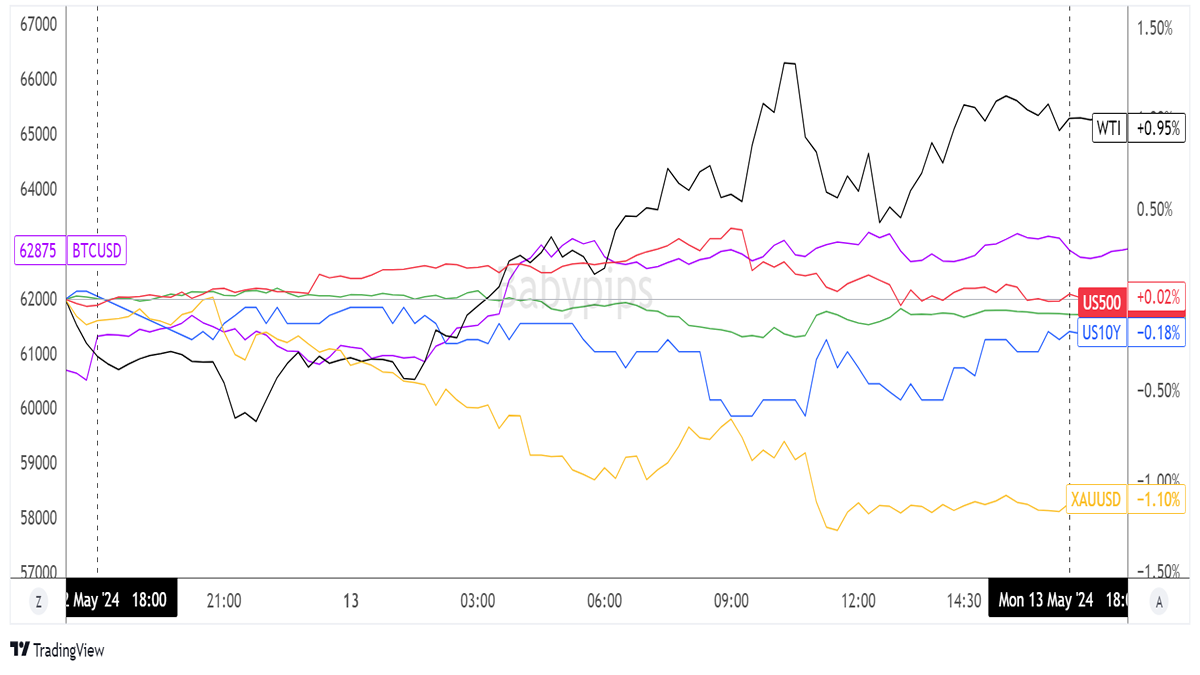

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

There wasn’t much on the docket in terms of top-tier economic releases to work with, leaving asset classes to look for individual catalysts and allowing investors to position ahead of major U.S. data this week.

Gold and crude oil were off to a wobbly start, but the latter managed to recover and close out nearly 1% higher for the day. As it turned out, the ceasefire in the Middle East is encountering challenges as Israeli forces reportedly continued to push towards Palestinian territory, reviving oil production concerns.

Bitcoin was also able to pare previous losses before stabilizing around $63,500 while U.S. equities struggled to find direction ahead of the U.S. PPI and CPI releases.

FX Market Behavior: U.S. Dollar vs. Majors

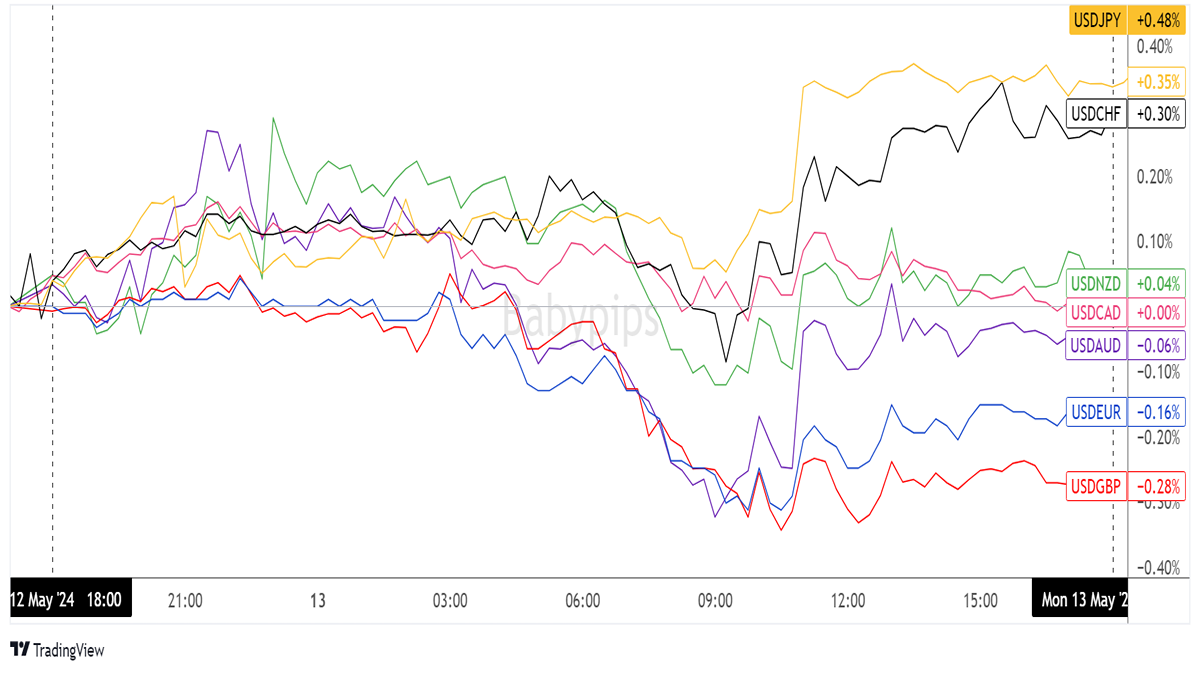

Overlay of USD vs. Major Currencies Chart by TradingView

Dollar pairs were off to a mixed start for the week, as EUR/USD and GBP/USD cruised sideways initially while comdolls tumbled from the get-go.

The Aussie seemed unimpressed by the NAB business confidence index while the Kiwi was likely dragged lower by dips in the BusinessNZ services index and quarterly inflation expectations.

Still, price action was generally sideways until the European session rolled along and spurred a clearer bearish tilt for the Greenback. From there, major currencies found their own groove once again, leading USD/JPY and USD/CHF to veer from the pack and chalk up roughly 0.30% in gains for the day.

On the flip side, the pound bagged the strongest gains against the dollar, as traders might be anticipating an upbeat U.K. jobs report on Tuesday.

Upcoming Potential Catalysts on the Economic Calendar:

- U.K. employment data at 6:00 am GMT

- Swiss PPI at 6:30 am GMT

- German and eurozone ZEW economic sentiment at 9:00 am GMT

- U.S. headline and core PPI at 12:30 pm GMT

- Fed head Powell’s speech at 2:00 pm GMT

It’s bound to be a busier trading day today, as the U.K. gears up to print its April claimant count change and possibly spark these moves from GBP/USD and GBP/NZD.

Later on, the spotlight shifts to U.S. inflation-related data, with the headline and core producer price indices lined up. Don’t forget to keep your eyes and ears peeled for Powell’s testimony, too!

Looking for your own spot to record your market observations & trading statistics? If so, then check out TRADEZELLA! It’s an easy-to-use

journaling tool that can lead to valuable performance & strategy insights! You can easily add your thoughts, charts & track your psychology with each and every trade. Click here to see if it’s right for you!Disclaimer: Babypips.com earns a commission from any signups through our affiliate link. When you subscribe to a service using our affiliate links, this helps us to maintain and improve our content, a lot of which is free and accessible to everyone–including the School of Pipsology! We appreciate your support and hope that you find our content and services helpful. Thank you!