The absence of fresh major market themes encouraged asset-specific price action on Tuesday.

Which major assets saw volatility and how did the U.S. dollar trade on a data-light trading day?

Headlines:

- RBA kept its rates unchanged at 4.35% and noted that the interest rate path “remains uncertain”

- Japan’s final au Jibun Bank services PMI for April rose from 54.1 in March to 54.3 in April and marked the highest since August 2023

- Switzerland’s unemployment rate remained at 2.3% as expected in April

- Germany’s factory orders for March: -0.4% (vs. 0.4% expected, -0.8% previous)

- U.K. S&P Global construction PMI for April: 53.0 (50.4 expected, 50.2 previous); “Overall rate of cost inflation was only modest,” “Another marginal reduction in employment”

- Euro Area retail sales for March: 0.8% m/m (0.6% expected, -0.3% previous)

- Canada’s IVEY PMI for April: 63.0 (58.1 expected, 57.5 previous)

- ECB member Joachim Nagel shared that factors such as improved supply chain resilience, labor shortages, and green transition could keep inflation elevated

- Fed’s U.S. consumer credit survey slowed from $15.0B to $6.3B in March as consumers pulled back on credit card use

Broad Market Price Action:

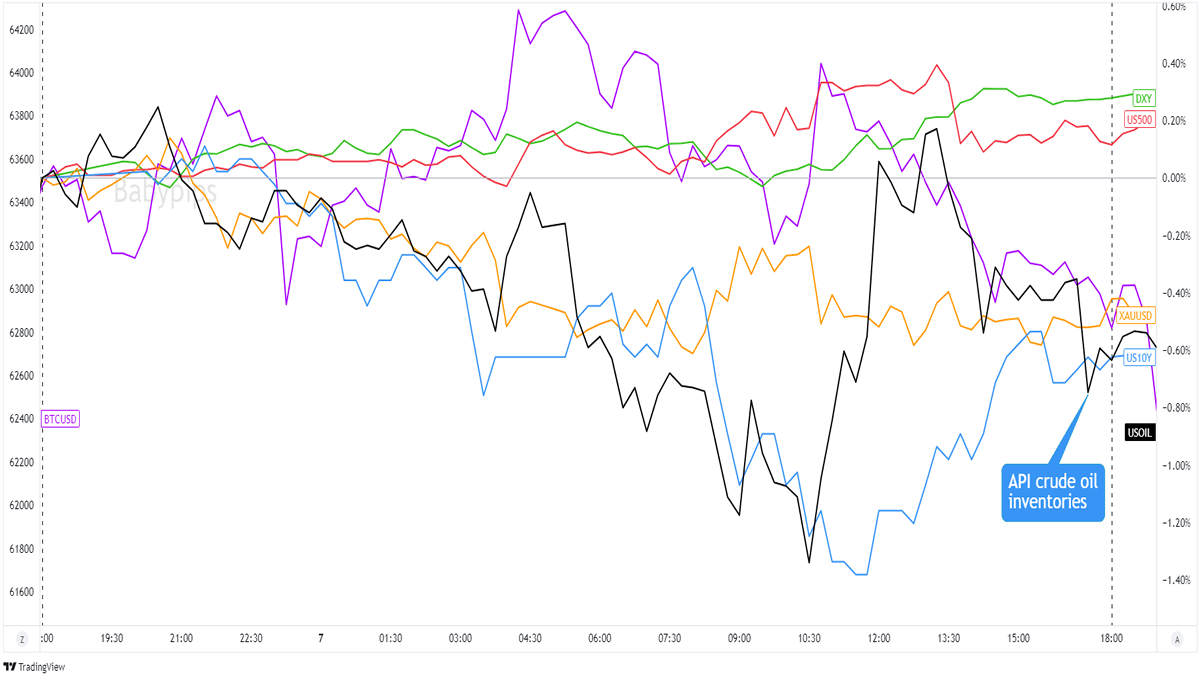

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

It was a mixed trading day for the major financial assets as the lack of fresh market catalysts encouraged asset-specific price action.

Spot gold lost more ground following a rejection from its $2,330 May highs and over the renewed expectations of a peace deal between Israel and Hamas. Ditto for U.S. crude oil prices, which also weakened as the perception of ample global supply outweighed the improving geopolitical concerns.

The S&P 500 managed to nudge a bit higher, fueled by hopes of a Fed rate cut and some pretty solid earnings reports. Meanwhile, the U.S. 10-year bond yields took a bit of a tumble to their lowest since early April as market watchers are eyeing the upcoming $125 billion in new bond supply this week.

FX Market Behavior: U.S. Dollar vs. Majors

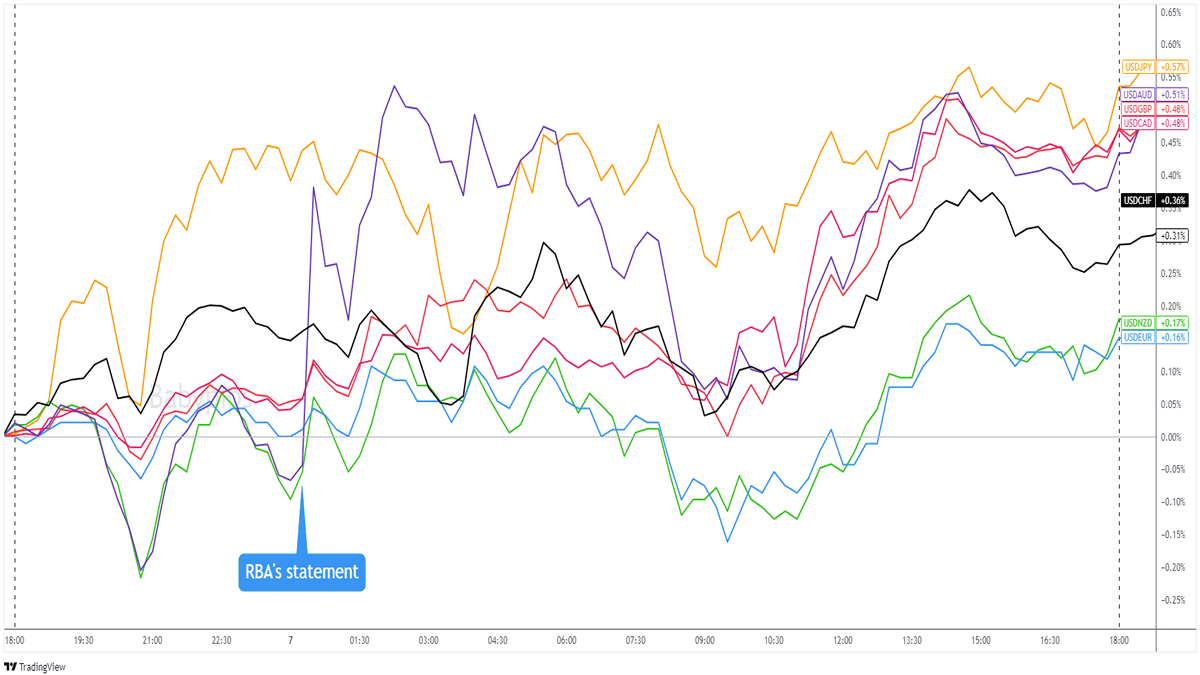

Overlay of USD vs. Major Currencies Chart by TradingView

The U.S. dollar traded in tight ranges for most of the day except for a bullish spike against AUD following a less hawkish than expected RBA policy decision.

The Greenback weakened a bit during the European session but saw improved demand during the U.S. session.

While there were no direct catalysts for the move, the dollar may have found support from decreased USD/JPY intervention concerns and traders pricing in not-so-dovish FOMC member speeches this week. Of course, it may have also helped that US 10-year bond yields pushed higher during the trading session and encouraged USD demand.

Upcoming Potential Catalysts on the Economic Calendar:

- Germany’s industrial production at 6:00 am GMT

- Italy’s retail sales at 8:00 am GMT

- U.S. final wholesale inventories at 2:00 pm GMT

- EIA crude oil inventories at 2:00 pm GMT

- FOMC voting member Philip Jefferson to give a speech at 3:00 pm GMT

- FOMC voting member Lisa Cook to give a speech at 5:30 pm GMT

- U.K. RICS house price balance at 11:01 pm GMT

- Japan’s average cash earnings at 11:30 pm GMT

- China’s trade balance out during the Asian session (May 9)

We have another light data calendar lined up, which ups the odds of tight ranges and volatility spikes around data releases. Keep close tabs on EIA’s crude oil inventories report as it could move crude oil prices. China’s trade data scheduled in the next Asian session may also influence overall risk sentiment so make sure you stay glued to the tube in case we see intraday trends!

Looking for your own spot to record your market observations & trading statistics? If so, then check out TRADEZELLA! It’s an easy-to-use

journaling tool that can lead to valuable performance & strategy insights! You can easily add your thoughts, charts & track your psychology with each and every trade. Click here to see if it’s right for you!Disclaimer: Babypips.com earns a commission from any signups through our affiliate link. When you subscribe to a service using our affiliate links, this helps us to maintain and improve our content, a lot of which is free and accessible to everyone–including the School of Pipsology! We appreciate your support and hope that you find our content and services helpful. Thank you!